Publication

Emerging Practices in TCFD-aligned Climate Risk and Opportunity Analysis and Disclosure

We interviewed 19 companies, conducted literature reviews, and collaborative workshops. […]

Climate-related financial risk encompasses several different types of risk.

Climate change can also present opportunities for companies positioning themselves for a low-carbon future, including expanded markets for existing products and services, new markets for new products, and cost reductions. The transition to a clean energy economy, and the worsening physical impacts of climate change, have all increased regulator and investor interest in understanding and managing climate-related financial risks.

To prepare for future climate scenarios and respond to increasing stakeholder pressure and potential regulatory actions, companies need to strategically identify the climate-related risks and opportunities unique to their business. Companies recognizing these risks and opportunities report on them in their corporate sustainability reports, voluntary reporting frameworks, and financial filings.

This process of identifying and communicating risks and opportunities to investors and stakeholders is called climate-related financial risk disclosure.

The Task Force on Climate-Related Financial Disclosure (TCFD) originally released its recommendations in 2017. These have since become the leading framework for climate risk-specific disclosure. TCFD has also taken steps to be interoperable with other sustainability disclosure efforts like CDP. Since the recommendations were released in 2017, a growing number of diverse companies have been working to align public reporting on climate-related risks and opportunities with the recommendations.

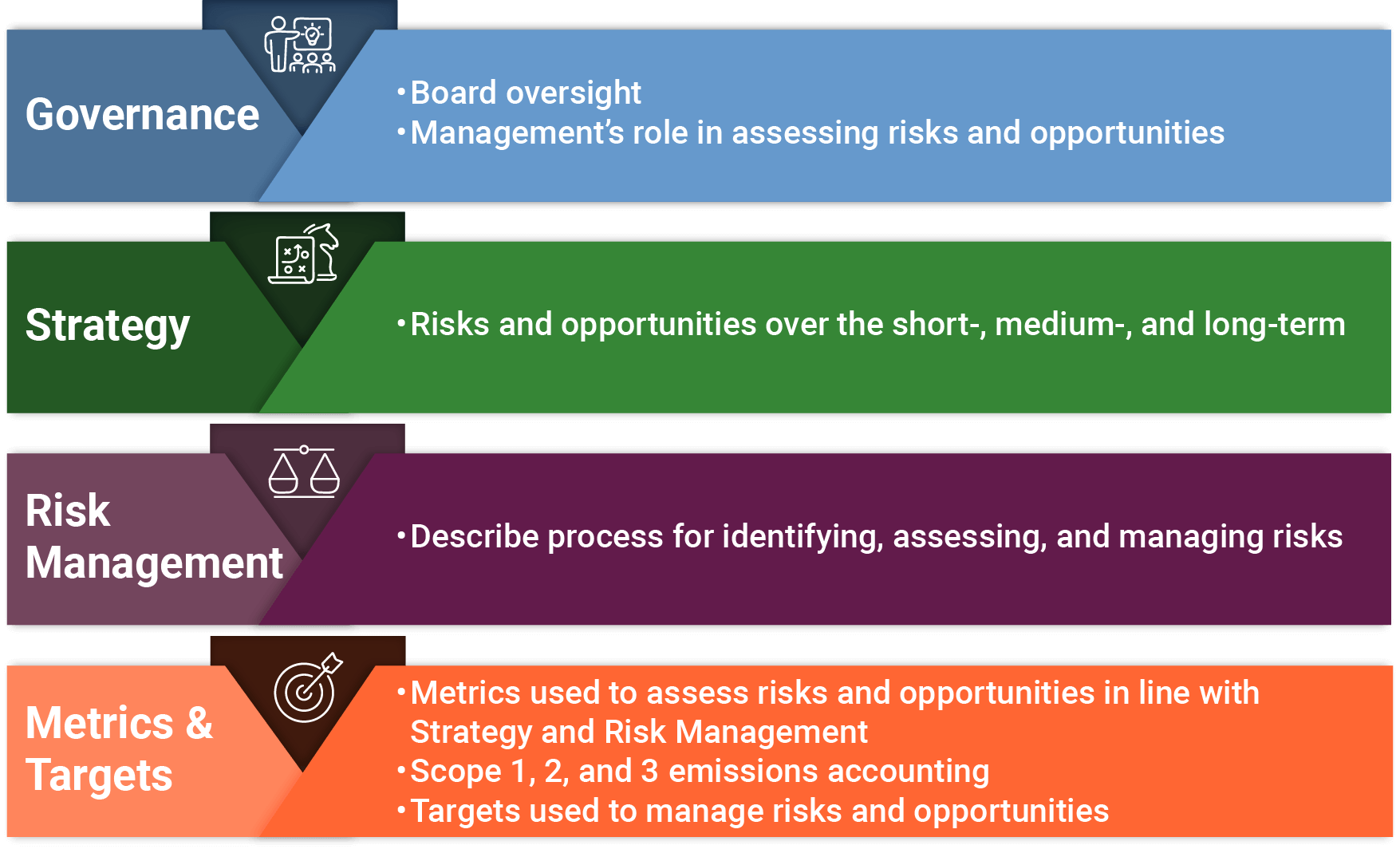

The TCFD voluntary reporting framework provided recommendations for how companies could disclose climate-related risks and opportunities across four areas: governance, risk management, strategy, and metrics and targets.

The recommendations include implementing guidance for companies on how to translate climate risks and opportunities into traditional financial terms—like revenues, expenditures, assets, and liabilities—and how to integrate climate risks into existing business continuity and risk management systems. A key recommendation is that more companies conduct a scenario analysis examining what climate change will mean for their facilities, operations, and supply and distribution chains, as well as demand for their products and services over a range of plausible scenarios.

In October 2023, the Financial Stability Board announced TCFD has completed its remit and asked the International Financial Reporting Standards (IFRS) to take over monitoring of the progress of company’s climate-related disclosures. The International Sustainability Standards Board (ISSB) incorporated the TCFD’s recommendations into its climate-related and general sustainability-related disclosure standards, which will now serve as a global framework for sustainability disclosures.

C2ES has supported the TCFD’s recommendations and seeks to enable better and more consistent climate-related financial reporting in the private sector. C2ES convened several workshops and webinars with companies leading up to the TCFD’s recommendations. In September 2017, C2ES issued a brief, Beyond the Horizon: Corporate Reporting on Climate Change, which identified areas where companies may require additional support in implementing the TCFD’s recommendations. One such area included helping companies use scenario analysis to assess climate-related risks and opportunities. Responding to this need, C2ES released a brief in August 2018, Best Practices and Challenges: Using Scenarios to Assess and Report Climate-Related Financial Risk.

Companies continued to discover new challenges and lessons as they began implementing the TCFD recommendations. They needed support translating information gleaned from climate scenario analysis into information that can be used for corporate decision-making. They also needed support assessing and disclosing the risks and opportunities related to the physical impacts of climate change, including how to demonstrate the financial value of resilience.

In response, C2ES hosted two workshops in 2019 that focused on these implementation challenges. In April 2020, C2ES released a brief, Implementing TCFD: Strategies for Enhancing Disclosure, that described the themes, lessons, and best practices from these workshops. In March 2022, C2ES issued additional resources, including a brief, Emerging Practices in TCFD-Aligned Climate Risk and Opportunity Disclosure, that examined how companies across sectors were successfully developing and reporting their climate risks and how to overcome barriers.

As research and policy action continue to evolve, C2ES is focused on how companies disclose their climate risks, how to support best practices in disclosure, and how the federal government can best assess and quantify climate risk in its own operations, and at an industry and sector level across the U.S. economy.