As energy demand rises and the global advanced energy economy continues its rapid shift toward electrification, batteries are becoming an increasingly central technology to the world economy. Presently, most batteries and critical battery materials are produced in China, but American technological innovation and industrial policy have put the nation in a strategic position to lead the next generation of battery development. Domestic production of critical inputs is crucial to developing a secure, resilient supply chain for batteries and preparing our manufacturing base for technological innovations of the future. Importantly, investing in a U.S. battery supply chain offers a tremendous opportunity to create jobs and promote economic growth in communities across the country.

Nowhere is this opportunity more clear than the Southeast United States. Since 2021 more than $48 billion has already been invested in this emerging “battery belt”, developing new manufacturing facilities for batteries, electric vehicles (EV) and stationary storage, and crucial inputs like cathode-active material and battery-cell production.1 Rhodium Group-MIT/CEEPR, Clean Investment Monitor (February 2026), https://climatedeck.rhg. com/clean-investment-us/manufacturing. Many of these investments were spurred by federal policy, which provided strong support for both the production and consumption of U.S.-made batteries and their components. However, recent revocations of federal support have put this industry in a precarious position and threatened the completion of the many announced investments across the region. Strong federal leadership, complemented by continued state leadership and a consistent policy environment, could make or break the success of the battery industry in the Southeast United States—and have major consequences for local economies and workers.

Since 2024, the Center for Climate and Energy Solutions (C2ES) has convened leaders across South Carolina, Tennessee, Alabama, North Carolina, and Georgia to explore the near-term opportunity for scaling this industry in the region, and to identify the remaining gaps that federal and state policy could help address to realize this potential. Across five in-person regional roundtables, hundreds of hours of stakeholder interviews, extensive background research, and economic analysis and modeling, C2ES has consulted more than 200 stakeholders to develop a clear picture of the opportunity in the region and produce a comprehensive policy roadmap to realizing the benefits. The following brief offers a review of the unique circumstances of the states and region and presents a policy roadmap with recommendations to federal and state policymakers, as well as industry leaders.

This brief is intended to serve as a starting point for further action, including supporting deeper policy engagement in the region and the development of additional enabling recommendations as new market opportunities emerge.

In the United States, batteries are at the heart of two key strategic sectors: energy and transportation. Under the United States’ stated goal of achieving “energy dominance”, stationary storage systems offer solutions to balance electricity supply and demand, enhance grid reliability, and provide crucial uninterruptible power supply for the rapid growth of data centers and manufacturing.2See Donald J. Trump, “Unleashing American Energy,” Executive Order 14154, Federal Register 90, no. 18 (January 29, 2025): 8353-8359, https://www.federalregister.gov/ documents/2025/01/29/2025-01956/unleashing-american-energy. In the transportation sector, as consumers continue to purchase electric vehicles at increasing rates and American automakers look to stay competitive in global markets, increased production of EVs and hybrids will require new stable sources of batteries and critical materials that are less exposed to geopolitical and trade risks. Building a secure manufacturing base is critical to the long-term health of the U.S. energy sector, and will require support for each stage of the battery supply chain, from raw material extraction through processing, material manufacturing, and battery assembly (see Box 1).

The lithium-ion battery supply chain begins with the extraction of raw materials in the form of ore or brine that contains lithium, graphite, nickel, cobalt, or rare earth elements. The raw material is then refined into chemical intermediates that can be manufactured into active materials that make up the different components of a battery. These intermediate battery materials include the cathode, anode, separator, and electrolyte, which are then used to fabricate battery cells. Battery cells are then assembled into battery packs for their end use as either stationary energy storage or to power electric vehicles. At the end of their useful life, these batteries can be recycled, and the component materials can reenter the midstream supply chain to be reprocessed into active battery materials. The entire supply chain is visualized in Figure 1, which also highlights (in yellow) significant gaps in the U.S. supply chain.

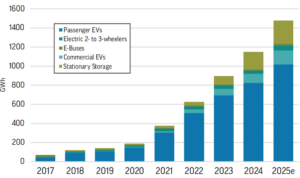

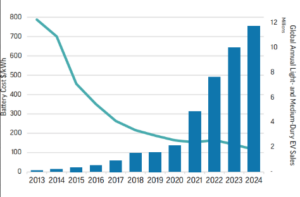

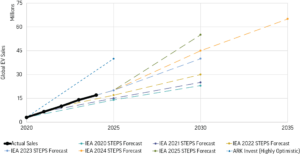

The global battery industry has grown rapidly in recent years. The late 2010s through the mid 2020s saw staggering growth in the global EV market, launching the battery sector into a new level of market commercialization. Globally, 20 percent of all light-duty vehicles sold in 2024 were EVs, up from 1 percent in 2017.3IEA (2025), Global EV Outlook 2025, IEA, Paris https://www.iea.org/reports/global-ev- outlook-2025.; IEA (2024), Electric car sales and sales share in the Net Zero Scenario, 2015-2030, IEA, Paris, https://www.iea.org/data-and-statistics/charts/electric-car-sales-and-sales-share-in-the-net- zero-scenario-2015-2030. 2024 was also a year of major milestones indicating batteries are on the pathway to price parity with existing technologies and mass-adoption readiness. Namely, annual demand for large-format batteries (such as those in electric vehicles and stationary storage installations) surpassed 1 TWh (see Figure 2), while the cost of a battery pack for an electric vehicle (EV) fell below $100 per kilowatt hour.4Lombardo, Teo et al., “The battery industry has entered a new phase – Analysis,” IEA, March 5, 2025, https://www.iea.org/commentaries/the-battery-industry-has-entered-a-new-phase. This growth trend for battery demand is expected to continue over the rest of the decade even under conservative scenarios, with current demand on a trajectory to reach 3.91 TWh by 2030 (see Figure 3).5Fleischmann, Jakob, and Martin Linder. 2025. “Global battery supply chain: Hidden regional trends.” McKinsey. https://www.mckinsey.com/features/mckinsey-center-for-future-mobility/our- insights/the-hidden-trends-in-battery-supply-and-demand-a-regional-analysis.

FIGURE 2: ANNUAL LITHIUM-ION BATTERY DEMAND BY APPLICATION

FIGURE 3: BATTERY DEMAND RISING WHILE PER KWH COSTS FALL

Taken together, this growth could indicate an inflection point in the long-term mass-adoption of this technology among emerging and developed economies. What is clear is that early-mover advantages, including the siting and location of supply chains, are solidifying across the broader battery industry in ways that will reverberate for years to come.

Battery energy storage deployment is experiencing its own boom, rising from 5 GW globally in 2020 to 104 GW in 2025.6Volta Foundation, 2025 Battery Report (San Francisco, CA: Volta Foundation, 2026), https://volta. foundation/battery-report-2025/. Between 2024 and 2025 alone, battery energy storage deployment achieved 43 percent growth globally and 53 percent growth in the United States.7Anna Darmani, Allison Weis, “Global energy storage market surpasses 100 GW annual installation milestone in 2025,” Wood Mackenzie (blog), January 13, 2026, https://www.woodmac.com/news/ opinion/global-energy-storage-market-surpasses-100-gw-annual-installation-milestone-in-2025/. Both of these end-uses—transportation and energy storage—provide lucrative export markets for the manufacturers able to supply them. Failure, or even delay, in taking steps to capitalize on the fleeting opportunity of the shifting market landscape threatens the future of both the existing American auto industry and emerging battery industry.

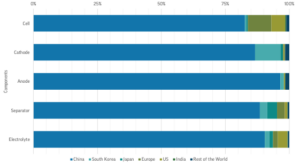

As the market has grown, major producers have consolidated to take advantage of the economies of scale for an advanced technology, positioning themselves to be massive beneficiaries of the long-term market trajectory. The consolidation of production with vertical integration of critical resources has led to a concentration of suppliers and manufacturing expertise to meet growing global demand. With many of these suppliers concentrated in China, other players are left scrambling to catch up and secure a portion of the battery market and the critical materials needed to power its development (see Figure 4).

While demand growth is expected to continue, challenges persist for companies looking to expand their share of the market through new manufacturing development, particularly in the United States. China maintains a tight grip on the global supply chain, from raw material production through final battery assembly. The top two global battery suppliers are Chinese, with China having produced more than 70 percent of all EV batteries ever manufactured.8Lombardo, Teo et al., “The battery industry has entered a new phase – Analysis,” IEA, March 5, 2025, https://www.iea.org/commentaries/the-battery-industry-has-entered-a-new-phase. This unparalleled market dominance presents a key barrier for new entrants into a market heavily reliant on economies of scale. However, for companies and local economies looking to diversify their investments to be less reliant on a single country of origin, this market offers an opportunity to attract investment, create jobs, and grow the local economy.

Figure 4 : LITHIUM-CELL AND COMPONENT MANUFACTURING CAPACITY BY REGION

The growing EV and battery manufacturing sector in the Southeast is beginning to scale in ways that could support the development of a multi-billion-dollar regional industry cluster. Final assembly for batteries has attracted companies producing components like cells and modules, as well as recycling companies that can process manufacturing scrap and end-of-life products. Further up the supply chain, mining and refining or production of critical anode and cathode materials ties the end-to-end supply chain together. As the region continues to invest in university research hubs, transportation corridors, energy infrastructure, and workforce development programs, a positive feedback loop will form in which industry actors are attracted to the systematic support for their sector.

To better understand how investments can ripple through the Southeast, C2ES commissioned a modeling effort by Greenline Insights. The model projects the economic impacts of a coordinated expansion of battery materials and manufacturing across the region by quantifying the jobs, income, and economic activity that could be captured locally. The analysis estimates the impacts of constructing and operating new facilities producing key battery components, including cells, cathode and anode active materials, electrolytes, separators, and aluminum and copper foils. In total, the modeled inputs represent roughly $102 billion in total investment from 2026–35 (in 2024 dollars). These inputs are designed to illustrate the scale of a coordinated supply chain buildout, not to forecast specific announced projects.

The scenario reflects an illustrative, policy-supportive trajectory for how a Southeast battery supply chain could scale over the next decade. It assumes a continuation of federal policy conditions in place through early 2025 that supported growth in electric vehicles, energy storage, and domestic manufacturing, representing an optimistic but reasonable demand outlook relative to more constrained policy scenarios.i

In this illustrative scenario, investing in the battery supply chain across the five-state region over the next decade would create 370,000 jobs, $60 billion in gross domestic product (GDP), $30 billion in labor income, and $140 billion in total economic output. Put in context (and adjusted for inflation), this translates to a roughly 140 percent return on investment for every dollar invested in this industry, illustrating the strong economic leverage of large-scale battery manufacturing and materials investments.

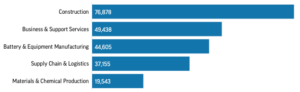

The largest areas of economic growth are concentrated in construction and battery manufacturing; largely a result of the capital-intensive nature of building and operating battery facilities. Upstream materials industries, including chemicals and related inputs, also experience substantial growth, highlighting the importance of materials production and processing in capturing the full potential value of the battery supply chain.

Job gains extend well beyond manufacturing (see Figure 5). In addition to construction and factory employment, growth occurs across supply chain and logistics activities as well as business and support services, including administrative services, professional services, and real estate, as investment ripples through supplier networks and local economies.

FIGURE 5: PROJECTED JOB GROWTH ACROSS KEY BATTERY SUPPLY CHAIN INDUSTRIES

While the needs of the growing industry may outpace the ability of any single state to meet them, as the industry continues to grow, state governments should lean into this opportunity. Proactive, collaborative strategies to support regional industry growth, including public-private actions designed to attract continued investment, drive innovation, and strengthen supply-chain resilience will be key.

The modeling support the importance of interconnected investment across the region, as a portion of each state’s individual economic gains are driven by activities in other state—an occurrence known as “spillover”. This is most pronounced in Georgia, where 14.5 percent of its total modeled growth stems from investments elsewhere in the region. This deep interconnection highlights the importance of a regional strategy to support the growth of this industry in a way that uplifts the economies of many states, rather than encouraging direct competition.

Supporting the growth of a critical battery material supply chain in the Southeast provides an opportunity to enhance the security of an industry that will be increasingly important to the global economy in the years to come. But major challenges remain for each segment of the battery industry. These problems include lag in downstream demand, barriers to fimancing for midstream production, and monopolies and bottlenecks for upstream raw material extraction and refining. Each requires bold solutions which need to be addressed simultaneously, and future policy support needs to take into account the interconnected nature of each step of the battery supply chain. Supportive federal action for the battery industry will demonstrate a strategic economic and national security interest in manufacturing these technologies domestically.

While global demand for EVs continues to increase rapidly, the American electric vehicle market is facing a slowing growth trend compared to industry expectations from just a few years ago. While growth in electric car sales fell from 40 percent in 2023 to 10 percent in 2024, sales of EVs in 2024 rose to 10 percent of all U.S. car sales as sales of gasoline-powered vehicles fell at the same time.9 Many battery companies made their facility investments based on the assumption that rapid U.S. market growth seen early in the decade would keep pace with global trends. The mismatch between growth in the U.S. and global EV markets has put American producers in a precarious position. Now, automakers and battery manufacturers are left wanting to expand capacity to keep up with global competitors and capture a share of this new consumer market, but unable to grow profitably due to lagging domestic markets.

Although forecasters expected 2025 would be a difficult year for the U.S. electric vehicle market, total sales remained relatively stable, falling just below 2024’s 1.3 million vehicles. The stability in final 2025 numbers was bolstered in large part by consumers looking to take advantage of EV tax credits that the One Big Beautiful Bill Act (OBBA) updated to expire in Q3 of 2025 rather than 2032 (see Figure 6).10 The forecast for the near-term U.S. market for electric vehicles, from 2026 to 2030, is much less clear. The premature expiration of the consumer EV tax credits represents a fundamental challenge for the U.S. battery industry: rapidly shifting and unpredictable long-term federal policy has made it difficult for businesses to make forward looking investment decisions to the degree needed to position themselves to take advantage of future market opportunities.

Growing electricity demand presents an additional shift in outlook for the battery industry. With the rapid rise in demand from data centers and other large loads, the market for batteries for energy storage is also growing at an accelerating pace. To make up for the lower-than-expected growth in the EV market—while taking advantage of the opportunity of serving the storage market—many U.S. battery factories have pivoted their focus to stationary energy storage. In late 2025, Ford and South Korean Battery Manufacturer SK ON made headlines by announcing plans to end their joint venture to produce EV batteries, splitting ownership of their Kentucky and Tennessee battery factories. 11 SK ON will take sole control of the Tennessee factory to accelerate their operations in the stationary storage market; they will still provide Ford with batteries for their electric vehicles, while diversifying their customer base to include stationary storage applications. Ford will take control of the Kentucky EV battery plant and repurpose its entire facility to make lithium iron phosphate (LFP) batteries for stationary storage units, a remarkable shift for the company as it looks to enter this new end-use market. Similarly, General Motors and LG Energy Solution announced plans in March 2026 to retool their Ultium Cells joint venture in Tennessee to produce batteries for energy storage systems.12 These plans include recalling 700 workers the company had previously laid off due to lower projected EV sales.

For battery materials manufacturers, uncertainty around demand for their products from downstream commercial customers creates a barrier to entry in the market. For this reason, certain battery material customers are looking to other markets to secure funding and offtake contracts. Especially among earlier-stage material producers who need smaller quantities of offtake to scale their production process, military and defense applications serve as a funding pathway to early-stage growth. However, total demand from the defense sector is not enough on its own to scale battery material production to the level needed to create mature and secure commercial markets.

The midstream makes up the bulk of the supply chain, encompassing the stages from production of precursor materials to the production of key battery components like anodes, cathodes, electrolytes and separators. The United States has gained a foothold in final battery assembly, doubling manufacturing capacity between 2022 and 2024 to 200 GWh of capacity with an additional 700 GWh under construction.13 However, battery manufacturing is only one stage in the value chain, while component manufacturing has developed much more slowly. The uncertainty around market growth for final products and battery manufacturers’ shifting focus toward stationary storage has disrupted the midstream market and left suppliers of these materials without clear or consistent offtake.

The failure to secure reliable offtake contracts limits companies’ ability to demonstrate the long-term certainty needed to enable investors to help scale their processes. Compounding this problem is the well-documented monopoly Chinese producers hold of critical minerals and battery materials, which both creates direct competition and disadvantages U.S. midstream companies in securing necessary critical mineral feedstocks. The economies of scale that Chinese producers have achieved provides a high quality and low price that cell fabricators have come to rely on. Even as U.S. policy increasingly encourages battery manufacturers to find new suppliers outside of China, new entrants to the market face a steep curve to replace these materials, where manufacturers require strict performance qualifications and comparable costs.

The expectation for instant quality and cost competitiveness is a challenge even for mature foreign entrants into the American market, such as Korean and Japanese manufacturers, due to comparatively high construction, equipment, and labor costs of producing the same materials in the United States that they already produce in their home countries. The problem is compounded for innovators looking to develop new battery materials and bring them to market. American battery startups are expected to jump from small, pilot-scale production to large volumes supplying commercial battery markets for EVs and stationary storage. There are very few niche commercial battery producers in United States, such as e-mobility or power tools, that have more manageable quantity and performance requirements than the consumer automotive industry. This leaves little opportunity for battery material manufacturers to gradually scale and improve their processes before selling into the demanding automotive sector. In the face of these challenges to operating in a nascent American market, many of these companies are unable to secure financing for their new facilities. This is leaving many aspiring suppliers on the sideline as cell fabrication and battery assembly ramps up in the United States.

The United States is heavily reliant on imports of foreign critical minerals necessary in the production of batteries. According to the 2026 U.S. Geologic Survey’s Annual Mineral Commodities Survey, the United States is solely reliant on imports for key inputs of battery materials, like natural graphite and manganese, and is highly dependent on imports of other key materials like cobalt, lithium, and nickel.14 These dependencies on foreign sources for crucial inputs to the manufacturing process for battery materials create supply chain bottlenecks and raise potential national security concerns.

In addition to mining, refining raw materials into precursors for battery materials presents another major barrier to integrated domestic supply chain development. Raw materials containing lithium, nickel, cobalt, and manganese must be refined into high-purity, useful formats serving as the building blocks of battery cells.

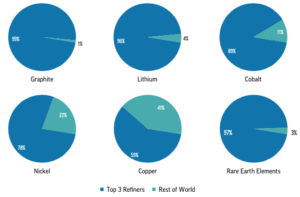

Currently, this process is concentrated in only a few countries, creating long and complicated supply chains that must run through specific geographic regions. For instance, 99 percent of graphite, 96 percent of lithium, and 89 percent of cobalt are refined by the top three countries refining that material (see Figure 7).15

However, the United States faces barriers to developing domestic mining and refining capacity necessary to address the existing over-reliance on foreign producers. In particular, long permitting timelines and lack of domestic geologic data limit the expansion on domestic mining. Refining expansion is similarly hindered by permitting and financing challenges, raw material availability, high electricity demand, and environmental concerns. The total extent of the United States’ mineral resources is unclear due to outdated geologic mapping of resources and a lack of funding to update this process, although efforts are underway through the U.S. Geological Survey’s recent Earth Mapping Resource Initiative.16 Such an initiative is critical not just for identifying the geographic location and quantity of minerals, but the concentration of those materials, which is often a more indicative measure of a project’s profitability.

For mining projects that do move forward, timelines for permitting of a new mine can stretch into a decade, often spanning multiple presidential administrations and business cycles in the industries they aim to supply.17 Those raw materials then need to be refined, but given the United States’ lack of refining capacity, they need to be sent abroad to do so. New refining capacity is similarly beset by permitting challenges, environmental regulations, and lack of technological and workforce know-how.18

The Southeast United States has emerged as a leader in attracting new battery manufacturing facilities. Of the nearly $112 billion invested in the battery manufacturing industry in the United States during the period 2021–25, approximately $48 billion (43 percent) went to five southeast states: Alabama, Georgia, North Carolina, South Carolina, and Tennessee.19 The region has been successful in attracting major battery manufacturing investments to date due to a combination of factors, including its conducive geography and geology, relatively low commercial electricity rates and land costs, research and innovation ecosystem, and deliberate efforts by state governments and economic development agencies to attract and support major new facilities. As these large investments have begun to populate the region, they have fostered the subsequent development of midstream and upstream industries ready to supply downstream battery manufacturers.

World-class research institutions and a workforce experienced in the automotive and aerospace industries create innovation and design advantages for these core manufacturing investments, leading to a positive feedback loop of growth as additional companies looked to site new facilities in prime locations. With access to export infrastructure including some of the largest deepwater ports in the country, facilities in the Southeast region are well positioned to supply American-made materials, components, and batteries not only to the domestic market, but also to meet rapidly growing global demand.

The geographic proximity of the southeastern states to one another, as well as to major population centers with strong consumer markets across the rest of the country, facilitates the development of an interconnected supply chain. This regional approach can maximize each state’s competitive advantages while allowing neighboring states to benefit from synergies that increase the market opportunity for the entire region. Battery and electric vehicle final assembly manufacturing plants in Georgia, for example, are well within a single day’s drive from nearly every other state in the region, while transportation corridors along major interstates 85 and 95 enable transport of raw materials and finished goods easily around the region. Deepwater ports in Savannah, Georgia; Charleston, South Carolina; and Mobile, Alabama, also offer ready access to export markets abroad.

The southeast region is also home to natural deposits of some key raw materials in the battery supply chain, namely lithium and graphite, although new mining is not yet operational for these materials. Once the planned mining and processing facilities are in production, this may provide a strategic advantage by building end-to-end supply from raw material production through final assembly.

The Carolina Tin-Spodumene Belt in North Carolina’s Piedmont region was mined for lithium from 1938–88, and mining company Albemarle is now in the process of reopening its Kings Mountain mine with plans to be operational by 2027.20 Nearby, Elevra Lithium (formerly Piedmont and Sayona) is developing its Carolina Lithium project, which will include both mining and processing for lithium hydroxide.21 On the other side of the Appalachian range, the Smackover Formation in Arkansas and Alabama contains millions of tons of lithium brine reserves, which have attracted development from companies like Standard Lithium, Exxon Mobil subsidiary Saltwerx, and Chevron.22 While there are other natural lithium deposits in the southwest United States as well—mainly in California, Nevada, and Utah—access to a potentially significant amount of lithium in the southeast, particularly if it is geographically proximate to active material production, could be a key competitive advantage for the region.

Another key material that could be mined in the region is graphite, an essential input to battery anodes. Presently, China controls 82 percent and 92 percent of graphite mining and processing, respectively, making this material of particular interest to American manufacturers and others looking to geographically diversify their supply chains.23 In the United States, Alabama contains one of the largest graphite reserves in the country, the Coosa graphite deposit in Coosa County, where Westwater Resources is developing a project to mine and process the material.24 In addition to natural graphite, several companies across the region are also building synthetic graphite production facilities, which use high temperatures to process other carbon inputs into battery-grade graphite.25 Examples of these in the region include Novonix’s facility in Tennessee and a planned facility by Anovion in Georgia.

Through the early years of battery industry’s development in the Southeast, states saw substantial competition among economic developers in attracting and landing new projects. Given the size and scale of many battery and EV facilities, the direct job growth and economic benefits can be transformative for states and local communities. As many large projects across the region have begun construction or opened production lines, the early-mover advantages they create are beginning to crystallize. As the industry scales in the region, there is a growing need for collaboration among states to fill in gaps in the supply chain that will complement the existing industry, rather than fueling competition for individual segments of the value chain.

Although there is not a singular formal cooperative agreement among the states in the Southeast to support battery industry, energy storage, or electric vehicle development, there are several existing initiatives that cross state lines. For example, the Mississippi-Alabama-Georgia Network for Evolving Transportation (MAGNET) is a tri-state research and innovation hub led by the University of Alabama, Mississippi State University, the University of Georgia, and Southern Company intended to “drive a coordinated approach to the advanced vehicle technology transition, stimulating a regional innovation ecosystem.”26

Another example is the Sustainability, the Southeast Electric Transportation Regional Initiative (SETRI). This initiative—managed by Duke University’s Nicholas Institute for Energy, Environment—unites more than 75 companies, utilities, nonprofits, cities, and academic institutions around common goals of promoting electric vehicle market development, conducting education and outreach to consumers and decision makers, and coordinating state transportation electrification efforts with university research.27

Each state in this region has specific competitive advantages and characteristics that define its unique opportunity within the supply chain. These are driven by the existing geography, industry, talent, and decades of strategic economic development planning that has shaped the state’s offerings and role. These profiles will outline where the industry in each state stands today, with major project announcements to date, and summarize the attributes defining the future of regional growth.

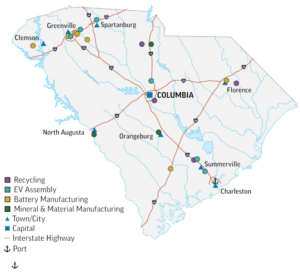

South Carolina has established itself as a hub for automotive manufacturing and innovation since the opening of BMW’s Upstate South Carolina Plant Spartanburg in the mid-1990s. This plant employs over 11,000 South Carolinians and catalyzed the development of a robust ecosystem of automotive manufacturers and researchers in the state.28 By 2030, BMW plans to manufacture six fully electric models at Plant Spartanburg.29 Additional auto manufacturers in the state have announced or expanded their operations to produce electric mobility options, including Scout Motors, Volvo, Mercedes-Benz Vans, and Oshkosh Defense.30

The electrification of the auto industry is driving a new set of suppliers throughout the battery supply chain in the state, drawing in companies serving the stationary storage market as well. On the battery assembly side, BMW’s Battery Assembly Facility is under construction to supply its growing line of EVs produced in Spartanburg. AESC has also restarted construction on its planned Florence EV battery manufacturing plant after a six-month pause due to economic and political uncertainty.31 Additional South Carolina-based battery companies supplying the stationary storage market include Enersys, Pomega, Fenecon, and sodium-ion producer Phenogy.

Amid this growth in battery manufacturing, a robust supplier network is developing in the state. Most notable is the recent completion of Redwood Materials South Carolina Campus, a historic $3.5 billion dollar investment to recycle used batteries and remanufacture critical inputs for the battery supply chain like lithium, nickel, cobalt, and copper.32

As the scale of the battery industry in the state grows, investment in research and innovation has followed. The University of South Carolina’s Carolina Institute for Battery Innovation (CIBI) was founded in 2024 to serve as a hub for research, development, and demonstration of new battery technologies and train the future workforce in this industry.33

CIBI is currently building pilot manufacturing lines to test and validate new battery cell production for researchers and industry partners, accelerating learning that drives new technology development from research to commercial

application.34 Key industry players including Siemens, EnerSys, and Phenogy will use the space to validate materials and production processes before scaling at their own facilities.

CIBI’s role as a testbed for new battery technologies plays a central role in the state’s designation as a tech hub by the U.S. Economic Development Agency. The 2023 creation of the SC Nexus for Advanced Resilient Energy, one of 31 Regional Technology and Innovation Hubs, set the direction for South Carolina as a leader in the United States’ goal to develop, manufacture, deploy, and export advanced electricity technologies.35

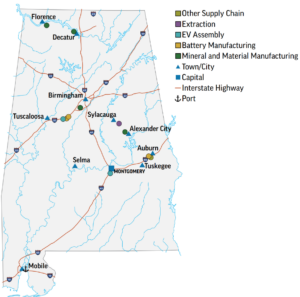

Alabama possesses several key assets that position it to play a unique role in a growing southeast battery belt. Alabama has a strong manufacturing base and experience in the automotive, aerospace, and defense sectors, all of which are set to become major demand drivers of battery technology.

The automotive sector in particular, the largest manufacturing sector in Alabama, will serve as an anchor for battery demand in the state and region. In 2023, Alabama became the top state for vehicle exports in the country, underscoring the industry’s importance to the state’s current and future economic prospects. 36 Alabama also has historical experience in chemical manufacturing, a sector with many similar workforce and infrastructure needs to the critical battery materials industry. The existence of strong battery demand pull, supportive infrastructure, and a workforce with the skills needed by the industry creates positive synergies in attracting new battery materials industry development.

Expertise in these core aspects of the battery supply chain afford the state an opportunity to capitalize on the growing global battery market. Alabama could be a good fit for suppliers to the battery industry who need workers, utilities, and regulators with experience in industrial and chemical sectors. Alabama also holds one of the few deposits of natural graphite in the United States, second in size only to Alaska’s Graphite Creek.37 This resource could provide a pathway to developing an integrated extraction and refining industry in the state, jumpstarting Alabama’s role as a supplier of critical battery materials. While the Alabama has not yet built out new industrial footprint in critical battery materials, the state and industry partners have demonstrated interest.

Alabama’s government agencies have identified the battery sector as a strategic opportunity and synergistic fit with the state’s existing sectors. Key players from the state’s economic developers, research universities, community colleges, workforce training providers, and utilities have joined together to form the Alabama Battery Team.38 This group is taking a holistic approach to economic development. They pitch companies on why they should locate their facilities in Alabama and provide all the support needed to successfully launch and scale their operations. This template is a unique strategy that considers many of the needs of a company to site and staff their new facility and should be considered as an approach for the entire region.

A key convener of this group is the Alabama Mobility and Power (AMP) Center, located at the University of Alabama. The AMP Center is a research and development hub that works to drive economic and workforce development in the EV, battery, and power ecosystem in Alabama and the broader region. To help achieve these ends, the AMP Center is establishing a battery research center on campus, which will host a pilot line for battery cell manufacturing to test and demonstrate the next generation of battery technology.

Georgia has been front and center in the southeast region’s emergence as a central player in the United States’ battery and electric mobility industry. In 2023, Georgia Governor Brian Kemp pledged to make the state the electric mobility capital of the world.39 To a large degree, the investment numbers over the first half of the decade set Georgia on a trajectory to compete for this title, anchored by investments from three electric vehicle original equipment manufacturers (OEMs): Hyundai, Kia, and Rivian. These auto manufacturers have brought in final battery manufacturing, including from Korean conglomerate SK Battery America, who opened its first U.S. battery factory in Georgia to supply Hyundai and other regional OEMs.

This strong base for final product manufacturing has firmly positioned the state as a demand driver for the entire battery and EV supply chain. Other midstream suppliers for anode material and electrolytes, two key components for battery cells, have announced plans to build facilities in the state. In total, Georgia has seen investment in the electric-mobility space rise to $27.3 billion since 2018, the highest of any state in the nation.40 This historic level of investment in downstream battery manufacturing is driving supply chain investment throughout the neighboring states in the region as well.

The rapid growth for the industry has underscored the need for accessible and flexible training of workers entering a new, rapidly developing industry with changing skill needs from its workforce. Georgia’s Quick Start program serves as a centerpiece of workforce development for new companies locating in the state, providing customized training through Georgia’s technical college system. Most recently, Georgia Quick Start opened the state’s first purpose-built EV manufacturing training facility to provide workers with the necessary skills to operate Hyundai’s advanced factory lines and work with high voltage battery systems.41

While workers develop the skills needed to manufacture the battery technologies of today, Georgia is powering a southeast research and development hub for the future of the battery industry. Georgia Tech is at the center of the charge with their Advanced Battery Center and Advanced Manufacturing Pilot Facility. These assets provide the city of Atlanta and local industry partners with world-class research facilities and shared infrastructure to test and translate innovations into commercial products. Atlanta can be a major regional innovation hub that attracts significant new company formation and manufacturing development.

One of Tennessee’s key advantages in the battery industry is its location at the crossroads between the Southeast battery belt and the traditional automotive capital of the United States in Detroit, Michigan.The growth of these two major manufacturing hubs provides a wealth of potential customers for critical battery materials. Tennessee is already home to three major auto OEMs: Nissan, Volkswagen, and General Motors. Nissan’s plant in Smyrna, Tennessee, was the center of North American production for the Leaf, the first mass-market electric vehicle.42 Volkswagen’s Chattanooga plant is the company’s hub for North American EV production with its own dedicated battery pack assembly facility.43 In 2021, GM announced a $2.3 billion joint venture with Korean company LG Energy Solutions to build a cell manufacturing facility in Spring Hill, which has since undergone a conversion to produce more cost-effective lithium-iron phosphate cell technology.44

In late 2021, Ford entered the state through a joint venture with Korean battery manufacturer, SK ON with plans to invest $5.6 billion in a revolutionary integrated battery and EV manufacturing plant in western Tennessee. This project was part of a broader strategic alignment across Tennessee and Kentucky around three battery plants, with two located in Kentucky. Due to uncertainty in the near-term growth of the American EV market, Ford and SK On ended their joint venture to increase flexibility in their strategic approach.45 As part of the split, SK On will assume full ownership and operation of the Tennessee plant with plans to continue supplying Ford with EV batteries while diversifying their customer base to include stationary storage markets.

While shifts in the national EV market have impacted the state’s EV manufacturing, the growth prospect for an advanced battery supply chain remains strong. In large part driven by the entrants of cell manufacturers to the state and surrounding regions, some of the United States’ largest electrode active material producers have set up production in Tennessee. On the anode side, NOVONIX, a synthetic graphite company, is expanding its operations in Chattanooga, Tennessee, with a second production facility to give the company a total production capacity of over 50,000 tons per year, making them largest battery-grade graphite supplier in the United States. Cathode active material producer LG Chem is also slated to open the United States’ largest cathode factory in Clarkesville Tennessee in late 2026. The company will produce high-performance nickel-cobalt-manganese cathode material with plans to expand its chemistry options as EV and stationary storage battery producers look to cut costs.46 Critical materials producers such as these should benefit from having increased potential customers due to the state’s position between two major hubs of battery and EV manufacturing.

North Carolina is a historical research and development hub for technological innovations, especially in the chemical and pharmaceutical sectors, providing valuable resources to help capitalize on new technical industries. The state has prioritized expansion into new growth opportunities in sectors relying on advanced manufacturing technology and workforce capacity, including semi-conductors and the battery supply chain. In 2023, the state made a splash by partnering with Toyota to locate its first battery manufacturing facility outside of Japan, with investment totals for the project reaching $14 billion.47 This facility will have 14 lines supplying batteries for both hybrid and fully electric vehicles and 30 GWh of annual cell production at full capacity by 2030. This magnitude of cell production will serve as an anchor for battery supply chain development across the state, serving as a major customer for battery components and critical materials.

North Carolina boasts a unique regional competitive advantage regarding critical materials used for battery production. The state’s natural hard rock lithium deposits offer an opportunity to secure an end-to-end supply chain for lithium batteries from mineral extraction through critical material manufacturing, cell fabrication, and final battery assembly. Two companies are developing new lithium extraction and refining projects. Albemarle’s King Mountain project will reopen a previously operating mine and refinery at an on-site processing facility to produce battery-grade lithium hydroxide.48 Elevra’s Carolina Lithium project is in the development stage for an open-pit lithium mine and integrated refinery.49

North Carolina is working to convene and coordinate battery supply chain companies to better understand the state’s strengths and identify ways to supercharge the industry’s growth. The North Carolina Battery Industry Partnership was funded by the state General Assembly through the NC Collaboratory grant program to provide insights into opportunities to strengthen the state’s economy, workforce, and energy system.50 This group’s convening work and forthcoming state roadmap will be a foundational step in preparing North Carolina’s battery industry to continue building on many of the state’s competitive advantages.

.

Although more than $48 billion has been invested in the battery supply chain across the region to date, significant gaps remain in the development of an end-to-end domestic value chain that touches each portion of the battery production process. Underscoring this challenge, conversations with stakeholders across the region highlighted that a more coordinated approach to supporting full value chain development is widely viewed as necessary for federal and state policymakers, economic developers, and investors, if the region is to develop a globally competitive domestic industry.

Although the region possesses natural reserves of lithium and graphite, and multiple companies are working to develop these resources, these projects are not yet operational at commercial scale and still face permitting, financing, and market hurdles. In addition to lithium and graphite, several minerals critical to the battery supply chain are not available to be mined in the Southeast region and must be imported. These include nickel, cobalt, and manganese, all crucial to one popular lithium-ion battery chemistry (nickel-manganese-cobalt, or NMC).51 Electric vehicle and energy storage battery makers are increasingly shifting to lithium-iron-phosphate (LFP) chemistries, which trade energy density for lower cost inputs that do not include minerals that face geopolitical and global supply challenges (like cobalt)—though the supply chain for LFP materials is even more heavily concentrated in China than NMC.52

While companies are developing several facilities to mine and process raw materials in the Southeast, more capacity to refine these resources into useful precursor materials and produce cathode- and anode-active material are needed to support the scale of battery materials demand in the region. Globally, lithium and graphite processing are mostly concentrated in Asia, meaning that even raw materials mined in North America are often exported to other countries for processing into battery-grade materials.53 Adding further challenges, recent economic uncertainty and volatility in federal policy has been extremely disruptive to the developing domestic industry. Canceled grants and loans from U.S. Department of Energy have left numerous companies scrambling to raise additional capital to complete construction of new facilities, while shifting tariff rates and the loss of significant federal tax credits through the One Big Beautiful Bill Act have materially affected project financing, significantly altering companies’ present and future budget projections. In particular, the loss of the 30D Clean Vehicle tax credit and its accompanying domestic content provisions have reduced overall domestic demand for EVs while also removing incentives for automakers to invest in American materials sources rather than foreign ones.54

In addition to mining and processing virgin materials, battery recycling is an area of interest to industry and policymakers alike as a potential domestic source for battery materials. The 30D Clean Vehicle consumer tax credit treated domestically recycled materials as fully compliant with its domestic content provision, encouraging automakers to increase their focus on working with U.S.-based companies to secure these materials.55 Some recycling capacity, including Redwood Materials’ facility in South Carolina, is helping to utilize factory scrap to produce new battery materials that would have qualified under the domestic content provision.56

There remain many barriers to a fully circular U.S. battery supply chain, however, which would enable battery inputs to be fully recycled into new products rather than needing to mine entirely new materials and dispose of end-of-life batteries. These barriers include a lack of capacity to process black mass into usable cathode active material domestically (it currently must be exported to foreign processing facilities) and a lack of reliable recycling infrastructure to support a pipeline of end-of-life batteries into the recycling system.57 Federal hazardous waste transport regulations also significantly limit the ability of companies to transport damaged batteries to a recycler, raising costs, sometimes prohibitively.58 Finally, electric vehicle drivers are often unaware of proper procedures to ensure their end-of-life battery is ultimately recycled.

The Southeast is home to cutting-edge technology research centers and has produced innovative research and development for new technologies and production processes across the battery value chain. However, the region still lags behind other technology innovation hubs like Silicon Valley, which has long enjoyed a robust venture capital ecosystem. This has enabled the region to attract an unusually high volume of serial entrepreneurs and specialized global talent that have made it a global epicenter for risk-taking venture capitalists.

It has also created a regional cluster in which innovators, entrepreneurs, and investors are able to share knowledge and industry best practices despite competition between new market players. The Southeast, on the other hand, has a smaller and more conservative funding ecosystem that can make it harder for innovators to navigate the pathway from pilot to commercialization. In the battery and critical minerals industries, the Southeast’s robust academic excellence and legacy of experience in engineering and advanced manufacturing is already attracting startups looking for lower-cost, talent-rich environments in which to grow. Unfortunately, access to capital, including venture capital, still lags what is needed to fully realize the region’s potential as an innovation hub.

The battery materials industry also faces a particularly unforgiving path from pilot to commercialization. Often, processes to synthesize materials at lab-scale quantities must be entirely redesigned to produce pilot-scale quantities, and again to produce at commercial-scale volumes. Companies must design their product for the customer’s needs and strict technical specifications, not only what works best for their technology developed in a lab environment.

Additionally, testing for new battery technologies can be capital intensive and require access to specialized facilities, which is not feasible for many early-stage startups. One possible solution would be to develop a shared facility, or “test bed” that could be used by different companies to manufacture and test new products, including a pilot line and other expensive but adaptable infrastructure. CIBI at the University of South Carolina, Georgia Tech’s Advance Battery Center, and the University of Alabama’s AMP Center are all developing infrastructure to test new battery materials and cells at pre-pilot and pilot scale that will be foster collaboration between researchers and regional company partners.59

Even for established companies, securing financing for new battery and components manufacturing facilities can be particularly challenging. It can take months to years for purchasers to qualify new battery materials as “battery grade,” and this uncertain timeline hinders stable offtake agreements and can make investments too risky to financiers. For first-of-a-kind manufacturing facilities, new equipment must often be imported from other countries, raising the costs significantly and exposing the domestic facility to import tariffs, an additional capital cost in an already capital-intensive industry.

The battery industry is quickly evolving in the United States, with unique needs for talent to develop innovative technologies, manufacture high-precision products, and work safely around high-voltage equipment or hazardous materials. Growing investments to produce EVs, batteries, components, and raw materials in the Southeast will also require a large, adaptable workforce.

One of the challenges of developing the workforce of the future is predicting the needed skills not just in the near term, but across a worker’s entire career. Employers participating in our regional roundtables highlighted that knowledge of key disciplines like robotics, chemical engineering, and advanced manufacturing were highly useful to the growing battery workforce. However, they also highlighted that strong problem-solving skills and an ability to adapt quickly to new types of technologies or production methods were most important to long-term success. With relatively low unemployment in the Southeast presently, particularly in the rural communities where many new manufacturing facilities are coming online, the availability of a trained workforce poses barriers to scale.60

As the emerging U.S. battery industry is relatively new, skills training and certification programs for manufacturing facilities are often individually developed and purpose-built to suit the needs of the specific facility workers are directly training to support. This makes it more difficult for workers to transition between jobs within the industry, and may slow companies’ ability to train new workers as they are often reinventing similar trainings in partnership with local community and technical colleges. Initiatives like the Battery Workforce Initiative through the U.S. Department of Energy and individual programs at academic institutions across the region are working to develop open source, standard curricula to provide a direct pathway to certification for workers that is accepted by most employers.61 These are important steps toward developing a nationally-harmonized set of standards and qualifications that can unify the battery industry.

Roundtable participants also highlighted the need for K–12 curricula to integrate awareness around the opportunities in the battery industry. Growing familiarity with emerging technologies is key to begin building the interest that is foundational to the long-term talent pipeline for the industry. They emphasized that this should also include helping young students develop the competencies needed to succeed across all advanced energy industries, not only batteries.

This roadmap presents recommendations for federal, state, and industry actors. For each recommendation, the roadmap identifies the problem, presents policy changes, and explains how the recommended actions will improve the battery and critical materials supply chain in the Southeast. These recommendations were developed in collaboration with regional stakeholders throughout a series of in-person convenings across the southeast United States.

The coordinating power of federal agencies and programs can bring order to key development and deployment challenges of new technologies as stakeholder scramble to develop systems to support the industry. Federal support is needed to widen the path to commercial scale in the battery industry, which is necessary to secure American energy independence, critical supply chains, and domestic manufacturing.

The United States lacks manufacturing capacity at scale for most materials critical to battery technologies. The first American facilities to produce materials and components for batteries are more expensive than subsequent facilities because they must be purpose-built for their customers’ needs and lack the benefits of economy of scale that other mature industries enjoy. In particular, these facilities face challenges in sourcing specialized equipment to match their production processes and from growing construction costs as building materials and labor become increasingly expensive in the United States.62

Constructing or expanding facilities amid higher relative startup costs than foreign markets is further challenged by a lack of guaranteed product offtake in a rapidly developing North American battery materials market. Because the downstream manufacturing market is also relatively nascent in the United States, or previously committed to existing foreign suppliers, it is difficult for emerging American battery materials producers to secure guaranteed offtake contracts with customers. This hinders companies’ ability to secure favorable interest rates on financing, further driving up the costs of their production and hindering their ability to build out capacity altogether.

Utilize the Defense Production Act (DPA)’s existing authorities to accelerate domestic production and procurement of critical battery materials and technologies, including:

The DPA Fund must also be reauthorized with expanded funding, or its mechanisms must be replicated through a different legislative vehicle. For instance, the recently introduced SECURE Minerals Act of 2026 has proposed the creation of a strategic resilient reserve to stabilize critical mineral commodity markets.64

The federal government can smooth the path to scale through direct support to manufacturers for these high up-front costs in the form of grants, loan guarantees, and flexible non-procurement offtake support. A dedicated entity with flexible financial tools is needed to support both the build out of new facilities to supply markets while ensuring demand support for this first-of-a-kind battery material production in the United States.

The Defense Production Act (DPA) is a key tool to expand industrial capacity for industries critical to national security. DPA Title III provides funding, as appropriated by Congress, that can be used to offer loans, loan guarantees, or other financial assistance to purchase and install equipment, increase production yields, or qualify products.65 Recent use of DPA Title III has demonstrated the federal government’s willingness to use both supply- and demand-side support mechanisms to expand domestic critical material production.66 The most notable recent example of DPA funding is the Department of Defense’s multi-billion-dollar partnership with MP Materials in July 2025, which included an equity investment, a loan, a 10-year price floor commitment, and an offtake agreement to fund the expansion of rare-earth processing and permanent magnet production.67

This use of DPA funding to support capital investment and stabilize offtake demonstrates a novel federal approach to growing manufacturing for a strategically important material with an immature market. Similar approaches could be taken to scale manufacturing for other critical materials, such as graphite and lithium, whose global processing capacity is heavily concentrated.

However, current funding levels for DPA limit the scope of its use for projects in the critical battery materials supply chain. The fiscal year 2026 Defense Appropriations Act provides only $321.9 million for DPA purchases, which is potentially lower than just the annual payments for the price-floor commitment in the MP Materials deal if commodity prices fall.68 For this reason, the current funding levels for the DPA will be insufficient to support an industry-wide build out for new critical material production, rather than offer support for individuals projects.

An alternative option to utilizing DPA authority to support offtake is the creation of a specialized government entity with the flexible financial tools to stabilize and scale commercial critical mineral markets. The use of tools such as price floors, advance market commitments, and equity investments could help develop a secure supply for industries that rely on critical minerals and their derivative products, including the battery industry. Examples include the Strategic Resilience Reserve as created by the proposed SECURE Minerals act and Project Vault as created by a recent Export-Import Bank loan.69

Recent rapid swings in federal policy have put the U.S. battery industry into a precarious position, facing significant policy and market uncertainty that hamper development. Incentives passed through the Inflation Reduction Act of 2022—for instance, the 48E and 45Y technology neutral tax credits; the 45X advanced manufacturing tax credit; and the 30D clean vehicle tax credit—all provided tax incentives to support the domestic production and deployment of batteries.70 In particular, bonuses or outright eligibility percentage requirements for domestic content in the technology-neutral electricity tax credits and the clean vehicle credit were instrumental in supporting companies’ decisions to build U.S. production facilities for final battery assembly, cells, and electrode active material. 71 Many of these producers intended to directly supply EV batteries to comply with the 30D domestic content provision.

Now, since the passage of the One Big Beautiful Bill Act in 2025 that ended the 30D clean vehicle credit in September of the same year, there is no consumer-facing incentive to support the deployment of American-made large-format batteries.72 Without this additional incentive to promote consumer preference for domestically produced materials, electric vehicle and home stationary storage companies have little incentive to source higher-cost inputs domestically, a disadvantage for the emerging industry.

Establish and expand purchase, manufacturing, and deployment incentives for products containing domestically produced critical materials, such as:

Long-term certainty of the level of federal support, as well as the financial incentive for consumers to demand domestically produced battery products, is necessary to supporting companies’ ability to secure long-term investments to develop local manufacturing facilities.

New legislation in Congress could reinstate or update federal tax credits with a specific focus on incentivizing large-format batteries utilizing domestically produced materials. The Critical Minerals and Manufacturing Support Act 2.0, for example, was introduced in the House of Representatives in February 2026 to increase the value of the 45X manufacturing tax credit to 25 percent, extend the lifetime of the credit by ten years, and add additional eligibility for key battery inputs.73

Similar legislation could extend the 48E tax credit to 2041 and beyond, while maintaining or enhancing the domestic content bonus. Other legislation could establish an American-made battery consumer incentive, based on the specifics of 30D, to provide a refundable tax credit for consumers to purchase domestically-produced large-format batteries for home energy storage or vehicles.

It is exceedingly difficult for researchers to translate innovation from lab scale to commercial scale, in part because of a lack of physical infrastructure that could make this development possible. Especially in the battery materials space, sourcing new equipment to pilot and scale production is capital and time intensive; the research and development (R&D) costs alone are often prohibitively expensive for a single startup.

Additionally, companies are struggling with the need for a comprehensive, standard, and coordinated workforce development approach that would standardize career pathways across the emerging battery industry, while supporting a shared understanding of necessary skills and talent development pathways for workers entering the sector.

Form a Battery Manufacturing USA Institute under the Manufacturing USA umbrella. This institute would:

A central coordinating body focused on developing the battery manufacturing industry could help identify research needs and support pre-competitive R&D efforts, coordinate the use of shared infrastructure to maximize resources and accelerate technological development, and support industry-wide workforce development pathways.

Manufacturing USA is a public-private partnership operated by the National Institute of Standards and Technology (NIST) in the U.S. Department of Commerce.74 It includes a network of 17 institutes focused on supporting manufacturing innovation, workforce development, and the build-out of a domestic supply chain for key advanced manufacturing products. For example, PowerAmerica—centered in Raleigh, North Carolina—focuses on accelerating the adoption of advanced semiconductor components. To date, none of the institutes is specifically focused on battery development.

To create a new institute, a federal agency launches a funding opportunity to award a consortium lead for a new institute to address a critical need or gap. Then, other organizations may submit proposals and, when selected, convene many partners across the ecosystem. In this case, the U.S. Departments of Energy and Defense should collaborate to support the development of this new institute, in recognition of the critical role the battery manufacturing industry plays to both the nation’s energy systems and national security.

To elevate the cutting-edge innovation and workforce development already being done by universities, companies, and other partners across the Southeast,this institute should be centered in the Southeast region, ideally at one of the existing battery research centers, and encourage complementary development among leading efforts. This institute would serve as a central coordinating body, led by industry and supported by federal funds and expertise, that could elevate the disparate research and development, workforce development, and manufacturing process improvement efforts across the country.

There is no office in the federal government that aggregates battery safety standards and resources, making it difficult for policymakers and communities to navigate the many competing sources of information. Several global organizations, (e.g., the National Fire Protection Association (NFPA), the Society of Automotive Engineers (SAE), and UL) set voluntary safety standards for the design and safe handling of batteries, but no coordinating body exists in the United States to centralize these many standards and resources.

Additionally, particularly for small communities new to energy storage, it can be challenging to interpret safety standards around battery installation and operation when determining local zoning and deployment best practices. A federal office that centralizes safety resources and standards and provides educational materials for a variety of audiences is necessary. Such an office could connect policymakers, employers, and the general public to crucial information to smooth the path to development of the battery industry.

Establish, in consultation with NFPA, SAE, and UL, an Office of Battery Safety within the U.S. Department of Energy to aggregate safety resources such as design or deployment standards and education resources for policymakers, companies, and consumers to interpret them. New standards and resources endorsed by this office should be approved by a panel of technical experts to ensure they are scientifically rigorous and high quality.

The U.S. Department of Energy’s Office of Environment, Health, Safety, and Security already houses its Technical Standards Program, which promotes the use of voluntary consensus standards.75 These may include safety standards for nuclear facilities, explosives, and fire protection, among others. However, there is no comprehensive resource for batteries, and those safety standards are generally limited to operational safety.

A similar program or office should be created within DOE with an explicit focus on battery safety. This office should aggregate technical and safety standards for batteries and include resources in plain language to better facilitate their interpretation by communities, employers, and policymakers.

This office could be created by action within the agency itself, or at the direction of Congress through legislation. To support the durability and impact of this office, funds should be appropriated to support its creation, maintenance, and administrative capacity.

Additional coordination of local efforts, as well as increased regional ambition, is necessary to support the development of the industry in the region. States across the Southeast are in the position to enact policy tailored to the specific needs of their businesses, institutions, and communities. Each of these recommendations should be implemented to elevate the individual characteristics of each state and the existing organizations operating within them.

The Southeast lacks the critical mass of investors to commercialize new battery technologies being developed at regional research institutions and labs, especially at the pre-seed stage where expert advisors are needed to help form startups. Furthermore, the current diversity and size of potential U.S. offtakers are insufficient for battery innovators to sell their product and raise revenue.

Few companies have been able to make the jump from pilot- to large-scale manufacturing without significant financial or technological support at the stages in between to demonstrate and scale their process.

Even for larger-scale manufactures who have proved their processes and validated their products, securing low interest loans to fully finance new facility production lines is a major barrier to development, particularly in the battery supply chain with high capital intensity and long return timelines. The Southeast is beginning to develop an expansive regional industrial cluster for battery and critical materials, but states across the region will need to combine resources and collaborate to become competitive in an increasingly mature global industry.

Create and fund a Southeast Energy Finance Authority (SEFA) to:

Several states across the United States have established new quasi–public-private financial institutions that use private sector tools to achieve public sector goals. These institutions, often known as innovation banks, infrastructure banks, or green banks work to deploy clean energy projects and improve energy infrastructure. Multiple institutions already operate across the Southeast to deploy advanced clean energy projects and upgrade critical energy infrastructure and industrial sites to attract new manufacturing.

In North and South Carolina, the Clean Energy Fund of the Carolinas provides affordable finance for clean energy projects across the two states. In Alabama, the recently established Alabama Energy Infrastructure Bank will provide financing to prepare sites for new facility development, improve energy infrastructure for new manufacturing, and leverage state funding to attract private investment. 76 These organizations provide a template for the types of financial support needed to support clean energy at the project and deployment level. However, an entity using similar tools but designed to support new company formation through commercial-scale manufacturing for a specific industry does not exist.

The financial mechanisms used by innovation banks would be a powerful tool to help crowd in private capital to scale the battery industry. At a larger scale, the Office of Energy Dominance Financing (formerly the Loan Programs Office) at the Department of Energy demonstrates the use of financial mechanisms to help reduce risks for private lenders investing in innovative projects. Combining these two approaches at the regional level could create a world-leading industrial cluster. Standing up this effort must start by identifying champions, ideally led by industry voices and representative groups, and accessing funding sources to capitalize this entity. One potential strategy to support this effort is the creation a specific financial mechanism, like a Special Purpose Vehicle (SPV), to pool investment from battery industry companies who will jointly benefit from specific supply chain and infrastructure projects in the Southeast region. SPVs have become an increasingly important tool to allow hyperscalers to jointly invest in new data center development while acting as separate entities to facilitate partnership and isolate financial risks.77

Alternatively, an interim first step could be taken by financing organizations already operating in the region, to aggregate demand for end use battery products manufactured in the region. This would provide certainty for producers, particularly the smaller producers still working to secure financing but in need of demonstrated long-term offtake.

Rapidly-shifting federal policy has left companies in the United States without a clear and consistent demand signal for batteries, and falling projections of EV sales have led U.S. battery producers to consider serving the growing stationary storage market instead.78 At the same time, states are navigating a rapid surge in electricity demand for the first time in decades, and are grappling with the challenges of quickly deploying affordable, reliable, resilient energy—challenges stationary storage systems are well-positioned to address.79

Working across state governments, public utilities commissions, and utilities, the Southeast region should set an ambitious energy storage deployment goal. To support achieving this goal, each state should also set a complementary state-level energy storage procurement target. These targets should include separate provisions for short- and long-duration energy storage solutions. Targets should prioritize domestically produced energy storage systems.

States with strong, clearly articulated goals to procure utility-scale energy storage will contribute to the clear, reliable, long-term demand signal needed to stabilize the stationary storage market. Setting a goal—especially one that is competitive with other states—helps to provide some of the long-term certainty producers need to underpin their investments into domestic facilities. Deploying energy storage on the grid at scale will require intentional planning and effort on the part of states, utilities, and grid operators; and serving this market will require longer-term certainty for companies in the supply chain.

Stationary storage is an important solution that can help to smooth peaks and valleys in power generation and demand throughout the day while providing backup power to critical infrastructure like hospitals in the case of extreme weather. New battery and long-duration storage installations can be deployed relatively quickly compared to natural gas generation and pairing them with existing and new solar or wind generation can help these intermittent resources be used to their fullest capacity while allowing ratepayers to benefit from the cost savings batteries can help generate.

Thirteen states already have state energy storage targets, including Virginia, with a target of deploying 3.1 GW of energy storage capacity by 2035.80 In addition to setting overall energy storage targets, multiple states differentiate between short-duration and long-duration storage in their targets, including California and New York.81 (The Virginia state legislature is considering a bill to add a specific long duration energy storage target and raise its overall goal.)82

In each state in the Southeast, a combination of executive leadership, action by the public utility commission in collaboration with utilities, and legislative support could be used to set an energy storage deployment target that would encourage the integration of storage resources into the electricity system, promoting grid reliability and bolstering system-wide resilience while increasing near- to mid-term certainty around regional demand for domestically-produced batteries and supporting local industry development.

Fragmentation of efforts to support the battery industry has hindered the ability to take a holistic approach to maximizing the local economic benefits of battery supply chain development. In many states, growing interest in battery development and deployment has led to several government initiatives hosted across disparate agencies. This may separate technical resources for battery manufacturers from safety resources for workers, which are also separate still from resources for communities evaluating options to site stationary storage.

Grants, loan programs, and consumer incentives that may be applicable to batteries, whether stationary storage or EVs, may be housed in different agencies across the state.

In each state, legislators should support a “Battery Storage Center” in collaboration with key industry partners, academic leadership, and state government for the purposes of centralizing collaborations in the state around battery storage deployment and supply chain development.

Examples exist for state action to enact or support energy-specific centers to coordinate efforts to develop an industry. In 2013, the Virginia state legislature created the non-profit Virginia Nuclear Energy Consortium Authority to support the commercialization of new nuclear technologies, foster public-private and cross-sectoral partnerships, and support the attraction of new businesses.83 In 2024, the Kentucky state legislature created the Kentucky Nuclear Energy Development Authority.84 The Authority is attached to the University of Kentucky’s Center for Applied Energy Research and works to support the nuclear energy ecosystem in Kentucky to grow the state’s economy, energy production, and advanced energy workforce.

Several states across the Southeast have launched research and development centers focused on supporting development in the battery industry. These centers of innovation include the North Carolina Battery Industry Partnership, the University of South Carolina’s Carolina Institute for Battery Innovation, Georgia Tech’s Advance Battery Center, and the University of Alabama’s Alabama Mobility and Power Center. Each of these centers serve to bring together industry, academia, and government to drive the industry forward through technologic, workforce, and economic development.