Take the corporate resilience self-assessment and receive your resilience profile. 24 questions. 6 modules. 15 minutes.

Physical climate risk has become a multiplier of every other disruption companies face—shaping earnings, insurability, financing costs, and competitive positioning. Yet drawing on interviews and dialogues with over 40 organizations, we found that most companies been unable to translate their recognition of the risks into readiness. While 65 percent of public companies now cite physical climate risk in their filings, only 25 percent of those acting have taken genuinely strategic measures to build climate resilience. Conversely, many companies continue to respond to event by event. The barrier is not information but the absence of shared financial language, clear ownership, and connected guidance. In this report, we call for a coordinated, practitioner-led effort to build that foundation—a navigable catalog of guidance, a maturity model, a standardized corporate climate resilience framework, and sector-specific playbooks—and we invite companies, investors, standard-setters, and expert organizations to build it with us.

Physical climate risk is no longer a tail risk—it is a threat multiplier that makes every disruption that companies experience harder to absorb. For instance, drought deepens supply shortages already constrained by tariffs, and wildfires or flooding compound existing economic uncertainty. Without adapting to the physical impacts from climate change, major companies globally face projected annual losses of $1.2 trillion by the 2050s.

Most companies recognize the risks but lack the organizational infrastructure to act on them at scale. Only 42 percent of companies in S&P Global’s 2025 Corporate Sustainability Assessment have adaptation plans, and responsibility is fragmented across sustainability, finance, and operations leaders who rarely share a common language or reporting line.

Translating climate risk into financial terms is critical to scaling corporate action. Companies that have quantified climate exposure as operational downtime, revenue loss, and value at risk, rather than describing climate risk more generally as high, medium, or low, are better able to mobilize investment. And among those that have invested in operational resilience, 82 percent report positive financial or reputational results, including stronger internal buy-in, better insurance terms, and improved access to capital.

We need a coordinated knowledge base and the shared infrastructure to move companies across industry sectors from awareness to scaled action, starting with a navigable catalog of guidance, frameworks, and tools; a corporate climate resilience maturity model; a broadly accepted standardized corporate climate resilience framework; and sector-specific playbooks. The building blocks exist—what is missing is the architecture to connect them. We are calling on companies, investors, and standard-setters to build that foundation together.

Physical climate risk is no longer a tail risk. It is a systemic risk shaping corporate performance in an environment defined by simultaneous disruptions, including geopolitical volatility, tariffs, supply chain upheaval, and cyber threats. Physical climate risk cuts across all of these risks and often compounds them. The question is no longer if disruptions will occur, but how organizations are building the capabilities, infrastructure, and technologies to adapt, compete, and deliver through them.

Against this backdrop, C2ES and Systemiq set out to answer the following key questions:

Over several months—through dialogues, roundtables, and first-person interviews—we spoke to over 40 organizations, including representatives from two dozen companies, and heard a consistent story. While many have begun assessing physical climate risk exposure and strengthening business continuity, far fewer are treating climate resilience and adaptation planning as a discipline with the power to shape strategy and deliver a durable competitive advantage. Without harnessing these strategic incentives, scaling climate resilience as strategy remains out of reach. Companies also lack a mechanism that enables them to combine and leverage the different available guidance, tools, and resources in a cohesive way that articulates the value of investing in climate resilience. These gaps matter. Investors, regulators, customers, employees, and communities are increasingly moving beyond asking only what risks a company faces. Now, they are asking how it will address those risks, how it will turn its response into a competitive advantage, and how it will build a more sustainable and resilient future.

There are some corporate leaders who are working toward decision-ready insights: They quantify downtime, revenue risk, and capital at risk; they consider climate impacts on people, infrastructure, operations, and value chains; they embed climate resilience into governance, operations, risk management, and capital planning; and they break down internal siloes and collaborate beyond their fence lines on the shared systems on which business depends. Still, these leading companies are few in number, and even they have struggled to scale strategies that work for them.

To advance beyond the current state of corporate climate resilience, we need more companies to assess the physical climate risks they face and translate that data into actionable insights. We need companies to understand where independent action is possible and where collective action across and within industry sectors is required. To achieve this, we need to move from qualitative exposure matrices to quantified, decision-ready risk and value-at-risk assessments; we need to expand from narrow continuity planning to enterprise-wide climate risk data and resilience strategies embedded in critical business functions (e.g., finance, operations, and governance); and we need to combine individual action with ecosystem engagement.

Building on the numerous preexisting tools, standards, and frameworks designed to support corporate climate resilience, we propose the following four practical ideas to enable further progress:

The opportunity to build a durable and adaptive competitive advantage is there for companies that embrace corporate climate risk and resilience as a strategic priority. Our economies and societies depend on it.

Awareness is no longer the biggest challenge: 65 percent of public companies now reference physical climate risk in their annual filings,1 First Street, The New Cost of Doing Business: How Climate Risk Impacts Operations, Earnings, and Enterprise Value (First Street, 2026), https://firststreet.org/research-library/the-new-cost-of-doing-business-report. and many more are taking one-off actions to reduce physical climate risks.2Linda-Eling Lee et al., The Hidden Adaptation Economy: A New View of Corporate Resilience and Opportunity (MSCI, 2026), https://www.msci-institute.com/wp-content/ uploads/2026/03/The-Hidden-Adaptation-Economy-A-New-View-of-Corporate-Resilience-and-Opportunity-260326_1.pdf. But recognition has not translated into enterprise readiness. S&P Global reports that only 42 percent of companies have adaptation plans, and fewer than half of those target implementation within the next decade.3S&P Global, Mercury Rising: European Entities Show Some Adaptation Gains as Physical Risks Mount, (S&P Global, 2026), https://www.spglobal.com/ratings/en/regulatory/delegate/ getPDF?articleId=3536929&type=COMMENTS&defaultFormat=PDF. Of companies that have begun to act, only 25 percent have taken measures that are “strategic” in nature (e.g., adapting products, services, or delivery models for climate impacts), while most remain focused on business continuity and engineering controls.4Marsh, Climate Adaptation 2025 Report (Marsh, 2025), https://www.marsh.com/en/risks/ climate-change-sustainability/insights/climate-adaptation-report.html.

Even where adaptation plans exist, most lack financial rigor. The central problem is valuation: Companies often cannot express the benefits of climate resilience investments (e.g., avoided losses, operational continuity, competitive durability) in terms that decision makers trust. Nor are the benefits—such as developing a durable competitive advantage—made clear. The structural mismatch between planning cycles and hazard dynamics compounds this problem: Corporate budgeting favors short payback periods, while physical climate risks evolve on multi-year timescales. An MSCI Institute survey of high-exposure companies finds that 68 percent assess physical risks over a two-to-five–year horizon, and only 10 percent look beyond a decade.5Linda-Eling Lee, Katie Towey, and Umar Ashfaq, What the Market Thinks: Findings from our Corporate Resilience Survey (MSCI Institute, 2025), https://www.msci-institute.com/wp-content/ uploads/2025/12/MSI-Corporate-Risk-Survey-231225.pdf. There is growing evidence that building climate resilience improves financial performance,6Niall Smith, “Does Physical Climate Risk Carry a Financing Premium?” Bloomberg Professional Services, October 15, 2025, https://www.bloomberg.com/professional/insights/ sustainable-finance/does-physical-climate-risk-carry-a-financing-premium. but until corporate resilience initiatives speak the language of the investments with which they compete, they will remain underfunded.

Additionally, companies often set a high bar for what counts as a financially material risk. When companies are willing to accept significant projected losses from physical climate risks, there is little incentive to invest in adaptation to avoid those losses. The dearth of laws and regulations for climate risk disclosure in the United States again compound this challenge. While more jurisdications globally are asking companies to disclose their climate risks, these requirements are often loosely defined. For example, the EU’s Corporate Sustainability Reporting Directive (CSRD) only requires companies to disclose financially material risks, leaving it up to the company to determine what level of physical climate risk it is willing to accept.7Directive (EU) 2022/2464 of the European Parliament and of the Council of 14 December 2022 Amending Regulation (EU) No 537/2014, Directive 2004/109/EC, Directive 2006/43/EC and Directive 2013/34/EU, as Regards Corporate Sustainability Reporting, OJ L 322, 16.12.2022, p. 15–80, para. 29.

Even if the challenges above were solved, it still would not be clear who “owns” climate resilience, or whether most companies have the capabilities and staff needed to act. Most corporate climate resilience efforts remain siloed and organized by risk domain: geopolitical risk often in strategy or enterprise risk, physical climate risk often in sustainability, operational risk in facilities. Each risk has separate owners, budgets, and governance, and the functions that assess physical climate risk, manage it, and finance it rarely share a common language or reporting line. Though climate resilience is often “real” at the facility level, where teams harden assets and refine response plans, physical climate risk is not a standalone domain; it is a cross-cutting threat multiplier that intensifies exposure across all these categories. In other words, companies that do not integrate—and then operationalize—climate resilience are solving an incomplete version of the problem.

Critically, responsibility most commonly sits with sustainability leaders who lack control over the levers that can strengthen climate resilience: capital allocation, procurement, and operations. There is rarely a top-down mandate that can drive enterprise-wide action. Companies often report that a senior-level leader is necessary to drive climate resilience across departments. Without an internal champion to coordinate and activate stakeholders and elevate climate resilience across the organization, implementation efforts may remain siloed.

Compounding these challenges is a lack of integration of climate resilience activity at the enterprise level. The MSCI Institute finds that 89 percent of large- and mid-cap companies show at least one hazard-specific resilience activity.8Linda-Eling Lee et al., The Hidden Adaptation Economy. But these are largely isolated efforts rather than part of a coherent strategy backed by clear priorities, realistic risk tolerances, and capital planning. Thus, the pattern that emerges is reactive: hardening assets after a wildfire or reassessing supply chains after a drought affects crop yields. Companies respond to each disruption individually but do not build the enterprise capability or management practices needed to absorb compounding and concurrent shocks to the systems on which they depend.

The range of frameworks, standards, tools, and analyses available to companies has grown significantly in recent years, but the landscape of guidance and legal requirements remains fragmented. Guidance is strongest for hazard identification, risk exposure assessment, and disclosure. It is weakest where companies most often get stuck: valuing climate resilience investments, connecting adaptation plans to capital allocation decisions, assessing very complex systems, building financeable pipelines of interventions, and coordinating action across organizational and sectoral boundaries. Some companies have expressed the need for new resources that can help them build climate resilience when they depend on other sectors or public infrastructure or help them navigate win-wins and trade-offs in efforts to both build climate resilience and decarbonize their operations and value chains. Guidance is also rapidly proliferating, often with limited input from practitioners, and no single resource provides end-to-end support, which means companies must piece together guidance from multiple sources, each developed for different audiences, sectors, and purposes. The transaction costs fall heaviest on the teams that most need help. The result is that many are unable to easily move beyond assessment and the initial steps of building climate resilience.

Companies themselves can be the most powerful catalyst for this work. Indeed, companies must lead in developing many of the tools that can forge a path forward. A more collective, practitioner-led effort is now needed to build shared infrastructure that can tackle the most critical problems in advancing climate resilience among companies across sectors. A map of existing frameworks, standards, and tools will make it easier to find the right resources in the fractured and complex guidance landscape. A holistic maturity model grounded in observable practice will help companies gain a better understanding of how well they are improving their climate resilience across their entire organization and provide clear next steps. A consensus-based standardized framework that coalesces existing resources and fills in any gaps, will help companies take coordinated, enterprise-wide action from risk assessment to implementation to decision-useful disclosures to their key stakeholders. Sector-specific guidance will provide companies with implementation-ready information that is tailored to the unique risks and challenges associated with their assets and value chains.

The most effective shared infrastructure in adjacent domains, from the Forest Stewardship Council’s common standard for sustainable forestry to the International Financial Reporting Standard’s adoption of the Task Force on Climate-related Financial Disclosures’ (TCFD) framework for climate risk disclosure, was built by practitioners who were willing to define what good practice looks like, test it in the real world, and share what they learned. When companies commit collectively to set public goals and road-test new approaches, the tools to implement those commitments improve more quickly. Transparency itself creates competition to demonstrate business leadership, driving adoption. We invite companies to share what works, help build the necessary tools that don’t yet exist, and make the path to robust climate resilience visible.

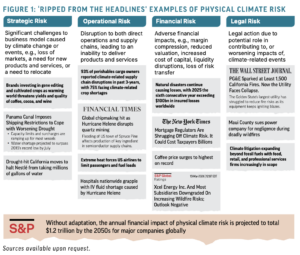

Physical climate hazards—heat, drought, flood, wildfire, storms, and sea level rise—are increasingly shaping corporate performance and testing corporates’ abilities to absorb and adapt to correlated, concurrent, and systemic shocks. Recurrent extreme climate-related events are now more an expected operating headwind than a tail risk.

The number of recorded weather-, climate-, and water-related disasters increased fivefold from the 1970s to the 2010s, and global economic losses increased sevenfold over the same period.9World Meteorological Organization, Rising Risks: Atlas of Mortality and Economic Losses from Weather, Climate, and Water Extremes, 1970-2019 (World Meteorological Organization, 2021), https://library.wmo.int/records/item/57564-wmo-atlas-of-mortality-and-economic-losses-from-weather-climate-and-water-extremes-1970-2019. NOAA estimates that 2024 alone brought the United States 27 separate billion-dollar disasters totaling about $182.7 billion in damages (and 23 in 2025).10 “Billion-Dollar Weather and Climate Disasters,” National Centers for Environmental Information, NOAA, https://www.ncei.noaa.gov/access/billions; “U.S. Billion-Dollar Weather and Climate Disasters,” Climate Central, https://www.climatecentral.org/climate-services/billion-dollar-disasters. Swiss Re estimates 2024 global economic losses from disasters at about $320 billion and insured losses at about $140 billion, leaving a substantial protection gap.11 “Hurricanes, Severe Thunderstorms and Floods Drive Insured Losses Above USD 100 Billion for 5th Consecutive Year, Says Swiss Re Institute,” Swiss Re Institute, December 5, 2024, https:// www.swissre.com/press-release/Hurricanes-severe-thunderstorms-and-floods-drive-insured-losses-above-USD-100-billion-for-5th-consecutive-year-says-Swiss-Re-Institute/f8424512-e46b-4db7-a1b1-ad6034306352.

These disasters are increasingly affecting corporate operations and driving earnings volatility. According to the MSCI Institute, more than 80 percent of companies report that extreme weather events have disrupted operations or added to operational costs in the past five years,12Linda-Eling Lee et al., What the Market Thinks. with large- and mid-cap companies experiencing average annual losses of $88 billion in asset damage and $1.1 trillion in business interruption.13 Linda-Eling Lee et al., The Hidden Adaptation Economy. A recent First Street report highlights that 65 percent of public companies now cite physical climate risk as a material factor in annual filings, more than double the share in 2001, and profit warnings triggered by extreme weather events have grown more than 6.5 times over the same period.14First Street, The New Cost of Doing Business. Additionally, 60 percent of the businesses who responded to WBCSD’s Business Breakthrough Barometers anticipate increased costs from physical risks within the next 12 months.15World Business Council for Sustainable Development (WBCSD), Adaptation Planning for Business: Navigating uncertainty to build long-term resilience, (WBCSD, 2025), https://www. wbcsd.org/resources/adaptation-planning-for-business-navigating-uncertainty-to-build-long-term-resilience.

These hazards create cascading impacts and risk across companies, not just for owned physical assets (see Figure 1):

Financial risk is also being reshaped by structural shifts in insurance markets, including rising costs, more restrictive terms, and widening coverage gaps. So-called “secondary” perils (e.g., wildfires, severe convective storms, floods) now account for 92 percent of global insured catastrophe losses,17Jerome Jean Haegele et al., Natural Catastrophes in 2025: The Persistent Rise of Wildfire and Storm Risk, Nat Cat sigma 01/2026, (Swiss Re Institute, 2026), https://www.swissre.com/ institute/research/sigma-research/sigma-2026-01-natcat-2025-wildfire-storm-risk.html. and the risks companies most need covered (e.g., non-damage business interruption, chronic and systemic risks, stranded asset value) are precisely those that remain largely uninsurable in any market. Compounding this, the insurance renewal process and enterprise risk management tend to operate independently in most organizations, meaning insurance coverage may not be updated in line with growing company risk exposure.

First Street finds that nearly 44 percent of companies say commercial coverage is too costly to fully protect their exposed assets, and one in four companies discloses reliance on self-insurance, meaning a growing share of climate-driven disruption is landing directly on corporate balance sheets.18First Street, The New Cost of Doing Business. An Aon-led report adds the insurer perspective: When companies fail to provide documentation of climate risk assessment and mitigation measures, 40 percent of insurers apply more conservative terms and 24 percent require additional internal review.19Natalia Moudrak et al., Underwriting the Future of Resilience: Developing Insurable and Bankable Infrastructure, (Aon, Global Infrastructure Facility, World Bank Group, IFC, and MIGA, 2026), https://www.globalinfrafacility.org/sites/default/files/2026-03/Aon_GIF_White%20Paper_ Insuring%20Resilient%20Infrastructure_FINAL_2.pdf. A large majority of insurers surveyed (76 percent) expect resilience measures to play a bigger role in underwriting decisions within three to five years.20Natalia Moudrak et al., Underwriting the Future of Resilience.

Companies that act to mitigate these risks can build real value. According to an MSCI Institute survey of high-exposure companies, among those that have invested in operational resilience, 82 percent report positive financial or reputational results, 68 percent cite increased investor interest, 67 percent report improved insurance terms, and 56 percent say they have secured better lending conditions.21Linda-Eling Lee et al., What the Market Thinks. Indeed, over the past decade, companies in the Dow Jones Industrial Average with insignificant rates of physical climate risk exposure have generated returns approximately 1.7 times higher than peers with moderate exposure,22First Street, The New Cost of Doing Business. a premium that reflects investors pricing operational resilience into long-term valuations.

Despite growing exposure and early evidence that investors seek to reward resilience to climate risk, most companies have not yet built the enterprise capability to manage physical climate risk as a strategic priority. The pattern we heard across interviews is one of recognition without readiness: Many (although certainly not all) companies accept that the risks are real, but struggle to translate that knowledge into repeatable decisions, funded investments, and measurable outcomes. For the few companies that had experienced catastrophic physical and financial impacts due to extreme weather, the experience spurred a build out of regional or corporate-wide strategies to address future risks.

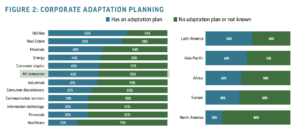

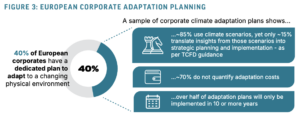

Many organizations have pockets of strong practice, traditionally grounded in engineering and business continuity. But S&P Global finds that only 42 percent of companies have shared adaptation plans publicly.23S&P Global, Mercury Rising; Paul Munday, Pierre Georges, and Catherine Baddeley, Risky Business: Companies’ Progress on Adapting to Climate Change, (S&P Global, 2024), https:// www.spglobal.com/sustainable1/en/insights/special-editorial/risky-business-companies-progress-on-adapting-to-climate-change. A recent S&P Global deep dive into investment-grade European companies found that none of the disclosed adaptation plans include advanced planning, such as adaptation targets, monitoring frameworks, or metrics to track progress.24S&P Global, Mercury Rising: European Entities Show Some Adaptation Gains As Physical Risks Mount. Of the companies that have begun to act publicly, only 25 percent have taken strategic measures (e.g., adapting products, services, or delivery models), while most remain focused on continuity planning, disaster response, or structural improvements to infrastructure.25Marsh, Climate Adaptation 2025 Report. Action thus far reflects where risks are most obvious: Utilities, real estate, and consumer staples lead, while healthcare, communications, and financials lag (see Figure 2 for a global view and Figure 3 for a deep dive into European companies).

A few caveats based on our discussions with companies can provide additional context. First, it is possible that more companies have developed internal climate resilience plans than is publicly known, as some of the companies with whom we spoke have developed them but have not disclosed them publicly.

Additionally, as not all plans lead to implementation, greater understanding is needed on how planning and execution are linked. Finally, for some companies, a lack of (or a rollback of) regulatory requirements to disclose climate risks and a lack of guidance for setting climate resilience and climate adaptation targets may also explain the current state of corporate climate resilience across sectors.

Across our interviews and practitioner dialogues, leaders described a widening gap between the pace at which climate hazards are changing and the pace at which corporate systems change. Physical climate risk does not arrive with a single owner: It presents simultaneously as an operational reliability problem, a capital planning problem, a supply chain problem, a workforce health and safety problem, and a customer and revenue continuity problem. As a result, even where strong technical assessments exist, many organizations lack the capacity, ownership, and cross-functional coordination needed to translate those assessments into concrete action.

A small number of companies are moving from hazard maps to decision-ready insights: quantifying downtime and value at risk, embedding climate resilience into governance and capital planning, considering worker safety, and collaborating beyond their fence lines on shared risks. But these leaders remain the exception. The more common pattern is fragmented, reactive, facility-level, and single-hazard focused; and it is increasingly insufficient given the pace and compounding nature of physical climate risk.

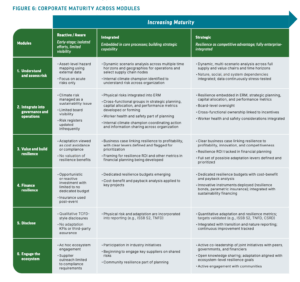

To characterize corporate maturity, understand gaps, and assess how existing guidance, tools, and resources can help companies integrate climate resilience at the enterprise level, this analysis is organized through the lens of six modules that are key to building climate resilience (see Figure 4). The modules build on frameworks others have developed (notably WBCSD’s Adaptation Planning for Business and Physical Risk and Resilience in Value Chains: CEO Handbook for Executive Engagement) while adding nuance drawn from our own practitioner interviews and research on what is needed to move from awareness to comprehensive action, and map to the key themes present in the frameworks, guidance, and tools we assessed (see “The Guidance Landscape: Valuable but Fragmented” on page 16).

The journey across the six modules is not strictly linear. Although some companies may follow the sequence described below, progress is most often iterative: Steps occur in different orders, capabilities develop in parallel, and setbacks in one module can reshape priorities in another. This organizing structure, while not prescriptive, provides a common language for diagnosing where both companies and the broader guidance landscape stand, what aspects of climate resilience remain stuck, and what it would take to enable progress across all aspects of implementing climate resilience.

The next two sections apply this journey first to the guidance landscape, and then to the state of corporate practice today, offering deeper dives on both for interested readers.

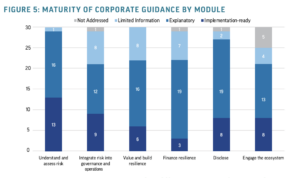

Across our interviews, climate resilience practitioners shared that they seek guidance that connects risk assessment to operating standards, investment decisions, and measurable outcomes across business functions. To understand what resources are already available, C2ES and Systemiq conducted a structured assessment of 30 frameworks, standards, tools, and market analyses, spanning international standards bodies, investor-facing frameworks, practical guidance from business coalitions, commercial risk analytics platforms, and independent research. These include (i) disclosure and reporting standards; (ii) management frameworks and technical standards; and (iii) analytic tools and market studies that translate climate science into decision inputs (see Figure 5). Appendix 1 lists all sources assessed, and Appendix 2 offers a heatmap of our anonymized assessment of the current corporate climate resilience guidance landscape.

Each resource was evaluated against the same six dimensions that structure the corporate climate adaptation and resilience journey, with the goal of mapping where guidance is mature, where it is still developing, and where gaps most affect companies trying to act on climate resilience.

This analysis examined standards that provide structured, end-to-end guidance for companies building formal adaptation planning processes; disclosure frameworks for communicating climate-related exposure; commercial analytics platforms that offer asset-level physical risk modeling; and investor-facing frameworks. The guidance landscape on corporate climate resilience has developed quickly; nearly all of the guidance materials included in our analysis were published in the last five years. However, these resources are not all oriented toward the same goal, and they do not map to each other in ways that guide a practitioner from one stage of the journey to the next.

The landscape is well-stocked with implementation-focused resources at the start of companies’ climate resilience journeys and progressively thinner toward the end, aside from a few more resources on public disclosure. The ecosystem reliably supports hazard identification, exposure assessment, and disclosure. There are far fewer resources available for valuing climate resilience investments in ways finance teams trust, connecting adaptation plans to capital allocation or financing mechanisms, building financeable pipelines of interventions, and coordinating action across organizational and sectoral boundaries. Few resources assessed provide tested, replicable methods for quantifying the return on adaptation spending or making the case for climate resilience capital in a corporate context and in terms that compete with near-term growth investments.

Since no single standard or framework provides end-to-end support, companies must piece together multiple frameworks, tools, and analyses, creating added work that requires connecting teams that rarely collaborate: risk, operations, engineering, procurement, finance, real estate, and sustainability. The transaction cost falls heaviest on the companies that most need support, and the gap between awareness and scaled action remains wide.

The tools and analytics platforms represent a rapidly maturing market but share a common limitation. Jupiter Intelligence, XDI, Moody’s RMS, MSCI’s Climate Value-at-Risk, S&P’s RiskGauge, and First Street offer increasingly sophisticated asset-level risk modeling, with outputs tailored to TCFD and ISSB disclosure requirements. But they are optimized for risk identification and quantification; they do not tell a company what to do with the results. That integration is largely left to the user.

To assess where companies stand across each module, we drew on practitioner interviews, industry convenings, and desk research. The maturity model prototype used here, summarized in Figure 6, reflects what we would expect to see at each level of practice across the six modules. A version of this model, developed further with practitioners, could become a practical tool for companies to assess where a company stands and identify next steps. A working prototype is available online.

The following steps can help companies move from reactive to strategic on climate resilience:

In our conversations with companies and our analysis of available data, most companies appear to have started to implement these shifts, but are not yet mature in their resilience efforts. Incremental progress is expected and should be viewed positively. Companies will move through this process in different ways and on different timelines, but eventually, the goal is for companies to be on the mature end in all modules.

Across the six modules, companies face limitations, not from a lack of information (companies are adept at acting on imperfect information), but due to the absence of the financial language, organizational ownership, and cross-functional infrastructure needed to turn information into decisions. These barriers, described below, will require improved methodologies, commitment from corporate leaders, and collective action to overcome.

This section provides a deeper dive into our findings, illustrated by vignettes from our interviews and practitioner roundtables.

Most companies have some awareness of their climate risk exposure, but many only have a qualitative understanding rather than putting risks into financial terms. Marsh finds that 78 percent of respondents conduct or are conducting identification, evaluation, and monitoring of extreme weather impacts: 40 percent assess risks qualitatively, 38 percent assess risks beyond a qualitative level, and the remaining 22 percent do not assess future extreme weather impacts at all.26Marsh, Climate Adaptation 2025 Report. The MSCI Institute’s global analysis of large- and mid-cap companies found that the three climate hazards most commonly driving corporate risk management activity are drought (65 percent of companies), flooding (57 percent), and extreme heat (43 percent).27Linda-Eling Lee et al., The Hidden Adaptation Economy. Rising insurance premiums and tightening coverage terms are themselves a signal worth incorporating into risk assessment, as they reflect insurers’ own views of asset-level exposure.

Interviewees consistently said that their organizations could characterize risk in terms of hazards but struggled to express it in operational and financial terms that match how executives make decisions. Companies commonly rank hazards on a scale of high, medium, or low risk to the company, which can be useful for identifying priority hazards, but is insufficient for capital allocation or supply chain redesign. An additional challenge is that different decisions operate on very different time horizons: Hardening a facility against flood risk is a near-term capital decision with relatively clear payback, while redesigning a supply chain for a 2-degree-C warmer world is a 10 to 20 year strategic commitment whose benefits accrue gradually, often to parts of the organization that did not bear the cost. The scenario analysis most companies have undertaken does not bridge this gap: even where scenario analysis is now standard practice for disclosure, the scenarios used are typically long-horizon and calibrated for external reporting rather than near-term operational decisions. Without a consistent set of organization-specific risk units (e.g., downtime, expected outage days, probability-weighted loss) applied across time horizons, different functions can reach different conclusions from the same signals.

Vignette: From hazard screening to quantified downtime

In a digital infrastructure-heavy business, leaders described moving beyond qualitative scoring by estimating operational downtime for critical facilities and translating that downtime into financial impact (i.e., revenue loss plus repair cost). They reported that this shift made climate risk understandable to asset owners and finance leaders, changing which interventions were prioritized.

How companies integrate resilience—and who owns it—varies significantly. Marsh finds that responsibility most commonly sits with sustainability leaders (54 percent) or risk leaders (28 percent), meaning the person nominally accountable for resilience rarely controls the levers that drive action.28Marsh, Climate Adaptation 2025 Report.Capital allocation and insurance usually sit with the chief financial officer (CFO).

Facilities hardening often sits with the chief operations officer (COO). Supplier continuity sits with procurement. Climate risk disclosure often sits with sustainability. Interviewees consistently highlighted that each function partially addresses physical climate risk within its own silo, but none covers it in full.

This is more than just a structural problem. It is a language problem. Each function operates with its own analytical framework: treasury manages risk through financial instruments and short feedback loops; enterprise risk management (ERM) through qualitative likelihood-and-impact registers on annual cycles; facilities through engineering standards and maintenance schedules; sustainability through disclosure frameworks and regulatory timelines. Even when risk signals are strong, they often fail to translate into coordinated action because the functions receiving those signals are working from different analytical starting points with no shared mechanism to reconcile trade-offs and connect them. Without a strong top-down mandate or a senior-level owner to drive cross-functional integration, enterprise climate resilience is structurally and linguistically difficult to achieve.

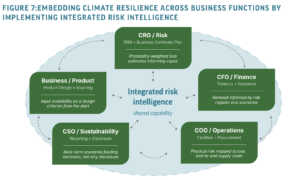

Figure 7 illustrates how climate resilience could be integrated into existing risk management infrastructure across different business functions through an integrated risk intelligence approach.

Vignette: Standardizing resilience as enterprise risk

One large organization described a nascent effort to make physical climate risk “just another standardized enterprise risk” where local facility and operations leaders across the organization use standard, scaled tools and data sources to identify and track risk. Today, identifying and tracking physical climate risk is still highly dependent on individual reporting methods and expertise, limiting scalability across regions.

Even when companies have climate resilience plans, many lack strategic and financial rigor and few link adaptation and resilience actions to core decisions, quantify costs and returns, or align timing with accelerating risk. The MSCI Institute finds that, while 89 percent of large- and mid-cap companies in the global MSCI ACWI index show evidence of at least one hazard-specific activity to build the resilience of internal corporate operations, fewer than half are selling products or services that help their customers build resilience.29Linda-Eling Lee et al., The Hidden Adaptation Economy. Forty percent of companies are not considering relocating assets or operations to reduce exposure to extreme weather.30Linda-Eling Lee et al., What the Market Thinks.

These findings highlight a key disconnect: resilience is being treated as a set of incremental risk controls rather than a value-creating strategic capability. As a result, investment decisions default to what is easiest to justify instead of what may be more material, leaving companies exposed.

In practice, the range of available interventions is broad.

The challenge is not a lack of options; it is the absence of a consistent method to compare and prioritize them against each other and against competing capital uses. And not every resilience action requires a major capital commitment: many valuable moves are operational shifts that can be taken incrementally, within existing budgets and approval processes. Progress along the maturity journey matters more than leaping to the most ambitious interventions.

Vignette: Reliability framing accelerates investment approval

A facilities leader described resilience investments getting internal traction when framed as reliability upgrades, especially when paired with near-term cost pressures such as rising energy prices, rather than as climate projects. The leader emphasized that anchoring the ask for a resilience intervention in core operational performance metrics could mean the difference between stalling and approval.

Only 60 percent of respondents in the Marsh survey believe they have sufficient money and resources to respond to future extreme weather impacts, while 40 percent do not.32Marsh, Climate Adaptation 2025 Report. Even among those planning increased investment, timing often stretches many years into the future. At an absolute level, private sector investment in adaptation remains limited (see aside),33CPI data show that adaptation finance reached an all-time high of $63 billion annually in 2021/22, though this remains far short of estimated needs. Tracked a adaptation finance is especially limited: CPI estimates annual average private adaptation finance at $4.7 billion for 2019–2022, up from a previously tracked figure of approximately $1 billion, and notes that actual flows are likely significantly higher due to severe underreporting. Climate Policy Initiative, Global Landscape of Climate Finance 2025, (Climate Policy Initiative, 2025), https://www.climatepolicyinitiative.org/publication/global-landscape-of-climate-finance-2025. and we suspect that the need is greater than what practitioners surveyed by Marsh estimate.34Climate Policy Initiative, Global Landscape of Climate Finance 2025.

In interviews, this showed up less as a denial of need and more as a capital-allocation and business-case problem. Because resilience investments compete with other projects, benefits are often framed as avoided losses, which are difficult to justify to finance teams. Additionally, funding for resilience investments is frequently episodic and reactive to a damaging event or a near miss rather than embedded as durable, multi-year programs. Several companies described having strong site-level engineering ideas but no clear mechanism to aggregate them into an enterprise portfolio, set investment thresholds, and protect budgets through planning cycles. Others pointed to insurance as a partial backstop, although many noted that rising premiums, higher deductibles, exclusions, and tighter terms make insurance less reliable.

This framing misses the competitive advantage story: Companies that build resilience ahead of their peers are not just avoiding losses, they are building the operational reliability, supplier relationships, and strategic optionality that become genuine sources of durable advantage as physical climate risk intensifies.

There is also evidence that lower physical climate risk exposure reduces financing costs for companies. A Bloomberg study of 2,900 companies found that those with 10 percent higher physical climate risk exposure faced a weighted average cost of capital 22 basis points higher than peers.35Niall Smith, “Does Physical Climate Risk Carry a Financing Premium?” Still, a recent finding from S&P Global Ratings notes that physical climate risk has driven rating actions on only about 1 percent of rated entities globally, attributing this to uncertainty about timing and magnitude.36Dr. Paul Munday, interview by Louis Woodall, Climate Proofers (podcast). Together, these findings suggest capital markets are beginning to price resilience into financing terms, even if the signal is not yet systematic.

Vignette: Capital markets can help fund resilience under the right conditions

A major financial institution described rising investor attention to physical risk and pointed to early market experiments, such as the Tokyo Resilience Bond, where resilience-linked structures attracted demand.* At the same time, they emphasized that labeled markets and resilience taxonomies remain inconsistent, creating challenges for scaling.

*“Tokyo Resilience Bonds,” Tokyo Metropolitan Government, updated February 27, 2026, https:// www.english.metro.tokyo.lg.jp/w/006-101-000968.

Vignette: Working with an insurer to enhance resilience

A large multinational described how their property insurer became a partner in their physical resilience program. The insurer connected the company with its in-house engineering team, which conducted site assessments and issued recommendations on vulnerabilities. When the company acted on those recommendations, it secured a reduction in its annual premium, creating a business case for resilience.

This model is gaining traction at scale. FM, a mutual commercial property insurer, has issued annual “resilience credits” since 2022. These are premium offsets that clients reinvest in engineering improvements identified by FM’s own technical teams. By 2026, the program had grown to $825 million, equivalent to a 10 percent premium offset for eligible policies, and had driven a potential reduction in economic impact of nearly $80 billion. The structure works because it aligns incentives: When clients reduce their risk profile, the mutual performs better, and those gains flow back to policyholders.*

* FM, “FM Announces Enhanced Resilience Credit of US$825 Million to Support Client Investment in Resilience,” press release, November 6, 2025, https://newsroom.fmglobal.com/releases/fm-a-nnounces-enhanced-resilience-credit-of-us-825-million-to-support-client-investment-in-resilience; Insurance for Good, “Resilience Credit for FM Clients: Q&A with Joe Dimitriadis,” August 21, 2025, https://www.insuranceforgood.org/blog/fm-resiliencecredits.

Risk disclosure is now an expectation for large companies, driven by expanding regulatory requirements and investor demand. In parallel, voluntary disclosure continues at scale, with nearly 23,000 companies now disclosing through CDP,37CDP, “CDP A List 2024: Only 2% of Companies Demonstrate Market-Ready Environmental Leadership,” press release, April 17, 2025, https://www.cdp.net/en/press-releases/cdp-a- list-2024. reinforcing the direction of travel even where requirements remain in flux.

A recent analysis covering the full MSCI ACWI universe—roughly $96 trillion in market capitalization—found that while 89 percent of companies have identifiable resilience activities, these activities are largely not visible through standardized reporting frameworks.38Linda-Eling Lee et al., The Hidden Adaptation Economy. Unlike emissions data, where 79 percent of listed companies now disclose and 60 percent have decarbonization targets, climate adaptation and resilience disclosures remain fragmented, often buried in operational descriptions rather than surfaced in structured financial filings.39Linda-Eling Lee et al., The Hidden Adaptation Economy.

Companies can become “reporting mature” without becoming “decision mature” if disclosures are not connected to management decision making. In interviews, teams described the “crosswalk problem”: building reporting architectures to satisfy multiple regimes while the harder work—agreeing on decision rights, setting operational thresholds, and embedding resilience into capital planning and procurement—lags. Several practitioners noted that disclosure deadlines create urgency, but unless CFOs and operational owners are accountable for underlying decisions and controls, reporting improves faster than resilience performance.

Across interviews, leaders emphasized that many of the largest risks and highest-return solutions depend on systems outside corporate control. Companies can harden facilities and strengthen continuity plans but still face material exposure when public infrastructure fails or disruptions cascade across shared supplier geographies (see aside). In our roundtables, leaders described a recurring “beyond our control” dynamic that can stall action.

Because these are collective-action problems, moving from awareness to action often requires pre-competitive cooperation—including, at times, with direct competitors—and sustained public-private collaboration to align incentives and invest in shared resilience. This is as true for supply chains as it is for physical infrastructure: When climate hazards threaten shared sourcing geographies, no single buyer can address the underlying risk alone. This requires companies to build new muscles and modes of engagement that can be unfamiliar but may be among the areas most ripe for innovation.

Vignette: Nature-based protection requires outside-the-fence coordination

A company operating large assets near a coast described working with external stakeholders on resilience investments. With these external stakeholders, the company was able to improve reliability by restoring wetlands to reduce storm surge impacts and other watershed-based measures. The story illustrates both the opportunity and the governance challenge: Outcomes depend on ecosystem and stakeholder coordination beyond the corporate boundary.

Vignette: Pre-competitive coalition tackles tropical commodity supply risk

A coalition of buyers of a tropical commodity faced a shared sourcing crisis: falling yields, climate-driven habitat loss, widespread farmer poverty, and fragmented, duplicative sustainability programs that were too costly to scale individually. Working together, they developed a centralized delivery platform to implement common environmental standards and coordinated agronomy, community welfare, and cooperative professionalization programs across shared supply chains. The effort unlocked significant joint investment, established a scalable operating model, and strengthened partnerships with governments and standard-setters. It illustrates a broader point: Supply chain resilience is often a collective-action problem that no single company can solve from within its own fence line.

Companies that recognize and assess their physical climate risks currently face dual challenges of implementing and integrating climate resilience at the enterprise level. Climate resilience efforts need to be coordinated across business units, rather than competing for attention and resources as a parallel climate program.

Companies need a clearer path from physical climate risk insight to strategic and operational action. They need guidance that works across sectors, aligns with evolving disclosure expectations, is realistic to implement for teams with limited time and capacity, and can connect climate risk to the geopolitical, operational, and financial risks that already sit on the board agenda. Making solutions clearer and more widely known among industry peers can encourage lagging companies to assess and begin to act on their exposure to physical climate risks.

Below we offer four ideas to help corporate leaders and the broader ecosystem make climate resilience more practical, comparable, and scalable. We recognize that there is already excellent work underway; the below is meant to build on that and focus efforts where there are opportunities to shift the field.

Even sophisticated companies struggle to navigate today’s crowded ecosystem. A practical first step would be creating a single source of truth that maps disclosure regimes, standards, tools, and sector references to concrete decisions; one that is built specifically for companies (a comparative starting point is the UN Environment Programme Finance Initiative’s (UNEP FI) excellent database of tools for financial institutions). Whether such a resource would be an all-encompassing meta-framework or a more streamlined navigator tool, it would need to be more than a library. It should point users to decision pathways (e.g., site selection, asset design standards, supplier resilience requirements, continuity planning, investment cases) with an indication of which tools and standards support each step. Such a tool would reduce duplication and help practitioners find what resources they need at their specific stage in advancing climate resilience in their companies. Our cataloging of current guidance is a first step; more work and additions from others as new resources are developed will be needed to make it practical and usable.

Many companies lack a clear entry point for what “good” corporate action on climate resilience looks like in practice (see aside). A holistic corporate climate resilience maturity model, developed with technical experts and corporate practitioners, could provide a simple way for companies to assess where they are on their climate resilience journey and how to progress. It would translate best practice into observable indicators across governance, strategy, operations, procurement, finance, and disclosure. These best practices could be, for example, including climate resilience as a regular topic for board review, procurement engaging critical suppliers on physical risk and mitigation, or capital planning including climate resilience thresholds and triggers.

As a prototype, we created an online corporate climate resilience self-assessment tool to begin the conversation with companies and key stakeholders, inviting discussion on how such a tool could be strengthened, updated, and widely used.

Over time, pairing the maturity model with benchmarking could help create a “race to the top,” giving companies a clearer sense of whether they are leading or lagging peers and where to focus investment and capability building. Such an approach also ensures that disclosures are closely tied to practices that work.

Organizations that already collect and standardize corporate climate data, such as CDP and the Science Based Targets Initiative (SBTi), could be logical partners to host such benchmarking, as could other actors focused on organizational resilience, such as the Federation of European Risk Management Associations (FERMA) in Europe.

A common framework for how to assess, integrate, value, and disclose decision-useful climate resilience measures in a corporate context would help align boards, executives, risk leaders, operators, and finance teams around the same questions: what climate resilience means for the enterprise, how it is measured, and how investments are prioritized. In practice, this implies converging on a small set of core measures (e.g., service continuity, downtime, asset criticality) and a consistent approach to quantifying both downside protection and upside value creation (e.g., reliability, customer trust, regulatory performance, strategic optionality). It also implies guidance on how to handle uncertainty and non-linear risks.

We need not start from scratch. One pragmatic way forward is to begin by coalescing the strongest elements of what already exists across disclosure regimes, risk methods, guidance on implementing climate resilience and adaptation, and emerging climate resilience metrics. Key gaps identified through that work could be addressed through a stakeholder process, ultimately leading to a holistic, overarching framework. That shared foundation could then support more targeted sector guidance and pathways, improving comparability while still allowing companies to tailor decisions to their assets, geographies, and operating realities. This approach could build on the experiences of other industry-led guidance processes, such as TCFD and TNFD.

The TNFD offers a useful process model here. It was developed through four iterative rounds of real-world piloting across more than 200 institutions, building credibility and adoption by incorporating practitioner feedback directly into each version. A climate resilience equivalent—piloted with companies across sectors, refined through iteration, and published with the backing of those who tested it—would carry far more weight than a framework developed in isolation.

Again, leveraging existing guidance would yield dividends. WBCSD published Adaptation Planning for Business – Navigating uncertainty to build long-term resilience in 2025, which provides an excellent “starter kit” for companies. It includes a structured process to set scope and goals, prioritize risks, design and score adaptation solutions, build and implement a plan, and monitor progress, alongside practical guidance on mobilizing internal support and a starter menu of measures.

The next frontier is making that guidance sector ready. Sector playbooks would translate the general adaptation planning process into industry-specific pathways outlining what works in a specific industry for specific assets. We are starting to see early movement in this direction. For example, the Resiliency Company, alongside JLL, Ryan, and the Urban Land Institute, developed a climate risk management playbook for commercial real estate,40The Resiliency Company, From Vulnerability to Value: A Risk Mitigation Playbook to Drive Resilient Development, (The Resiliency Company, 2025), https://resiliency.com/climate-risk-management-playbook. and Marsh generated sector-focused guidance on strengthening supply-chain resilience in the manufacturing sector.41 MarshMcLennan Agency, Manufacturing Risk Report: A Guide to the Critical Five, (MarshMcLennan Agency, 2025), https://www.marshmma.com/us/insights/details/ manufacturing-risk-report.html. However, most sectors still lack comparable, high-aspiration pathways that reference a common foundational framework.

After they are developed, these sector playbooks would then need to be paired with regionally-specific approaches. A recent report from the Council on Energy, Environment and Water (CEEW) lays out a detailed vision for this approach in the Indian context.

An additional illustrative example is the Mission Possible Partnership, which aims to accelerate the decarbonization of hard-to-abate sectors through shared sector “transition strategies” with common milestones across companies, finance, and policy makers. A climate resilience equivalent could help sectors agree on priority disruption scenarios, “standard moves,” and outside-the-fence collaboration needs. Then it could pilot, refine, and publish pathways that companies can pick up and use.

The companies that will perform best through physical climate risks and disruptions are the ones that have built the organizational capability to absorb shocks, protect continuity, and make confident decisions under uncertainty. Sophisticated climate models and detailed disclosure reports will not be sufficient.

Recognition of physical climate risk is growing among companies, but their readiness to respond to disruptions lags in pace and scale. Physical climate risk is already shaping earnings, insurance terms, financing costs, and competitive positioning, not as a standalone hazard but as a multiplier of every other disruption companies face. Three shifts remain incomplete across the corporate landscape: from qualitative exposure matrices to quantified, decision-ready risk assessments; from narrow continuity planning to enterprise-wide climate resilience strategies embedded in finance, operations, and governance; and from isolated action to ecosystem engagement. The gap between what growing climate risks demand and what corporate systems can deliver is widening, and most companies still lack a clear answer to the question that matters most: What do we do now?

Yet progress is emerging. A small but growing number of companies are moving from physical risk assessments to decision-ready insights, from facility-level hardening to enterprise-wide resilience initiatives, and from isolated action to cross-sector collaboration. These companies are beginning to break down internal silos and recognize that climate resilience is not a sustainability workstream—it is a core business capability.

Realizing that potential across industry sectors at a global level will require additional complementary, systems-level efforts working in parallel. For example, there will need to be improved leadership education that establishes a shared baseline on physical climate risk at the board level, investor engagement that rewards credible action with better access to capital, and place-based coalitions that bring companies, utilities and other infrastructure providers, local governments, and communities together to address shared regional vulnerabilities no single organization can solve alone.

Underlying all of these is the need for a shared foundation—a common language and methodology that enables companies to assess, value, and implement climate resilience consistently and at scale. That foundation does not yet exist in full, but building it is the essential next step. What is required now is the collective will to do so, and the transparency to share what works along the way.