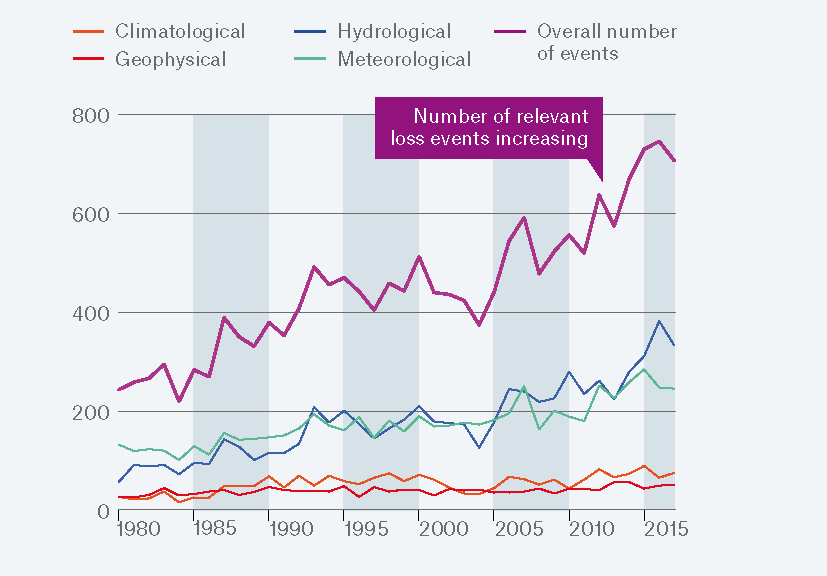

The greater frequency and intensity of extreme weather and chronic climate impacts impose real costs on communities and companies. Extreme weather causes property damage, disrupts business operations, and affects global supply chains across the economy. Sectors more closely tied to natural resources, such as agriculture or tourism, are particularly vulnerable to changing climate conditions. The re-insurer Munich Re estimates that natural disasters (most of which may be influenced by climate change) caused $340 billion in losses in 2017, with 83% of those losses coming in North America which had a particularly devastating hurricane season that year. Data from the company shows that the climate-related disasters are on the rise around the world.

Companies have always navigated a changing business environment. But now they face a changing physical environment, as climate change affects their facilities and operations, supply and distribution chains, electricity and water supplies, communities where they are based, and their employees and customers. In addition to the added risks of climate change, companies are expected to adjust for market opportunities that can be presented by changing needs for more climate resilient crops, materials, and technologies to support climate change mitigation and adaptation.

A June 2026 report from C2ES and Systemiq, drawing on interviews and roundtables with leaders from more than 40 global organizations, identified key gaps in the development and implementation of effective climate resilience strategies. While difficulties translating resilience into financial terms, fragmented guidance, and a lack of top-down leadership are key factors holding companies back from integrating climate resilience enterprise-wide, establishing a cohesive guidance landscape, shared baselines for progress, standardized corporate climate resilience framework, and sector-specific pathways to action are paramount to moving corporate resilience from awareness to scaled action.