A recent major funding announcement from the U.S. Department of Energy (DOE) highlights the importance of policy support in scaling climate technologies. The announcement came shortly after C2ES held the first meeting of a working group focused on engineered carbon removal. This is the first of four working groups focused on critical-path technologies: engineered carbon removal, sustainable aviation fuel, long-duration energy storage, and clean hydrogen. The working groups will provide a venue for communication and problem-solving across each technology’s ecosystem. Key outputs will include thought leadership, identification of synergies between technologies, and policy recommendations to enable deployment and commercialization.

The DOE awarded $1.2 billion on Aug. 11 to regional direct air capture (DAC) hubs in Texas and Louisiana. In addition to the two projects along the Gulf of Mexico, DOE intends to award $99 million for 19 projects supporting feasibility and front-end engineering and design studies for potential DAC hubs across the nation. DAC hubs can enable large-scale deployment and reduce overall costs by locating multiple direct air capture projects in a region where they share infrastructure. The department will also spend $35 million on carbon removal purchases to support long-term demand.

These announcements build on the bipartisan infrastructure law’s support for DAC hubs and the Inflation Reduction Act’s 45Q tax credit. All these initiatives will collectively contribute to the DOE’s efforts to capture carbon dioxide from the atmosphere and store it safely at gigaton scale for less than $100/ton within a decade, under its Carbon Negative Shot.

Carbon removal is not a substitute for reducing emissions. However, achieving net-zero or negative emissions will require large-scale deployment of new technologies, including tech to remove the excess carbon in the atmosphere generated over the past 200 years.

Technology Working Groups

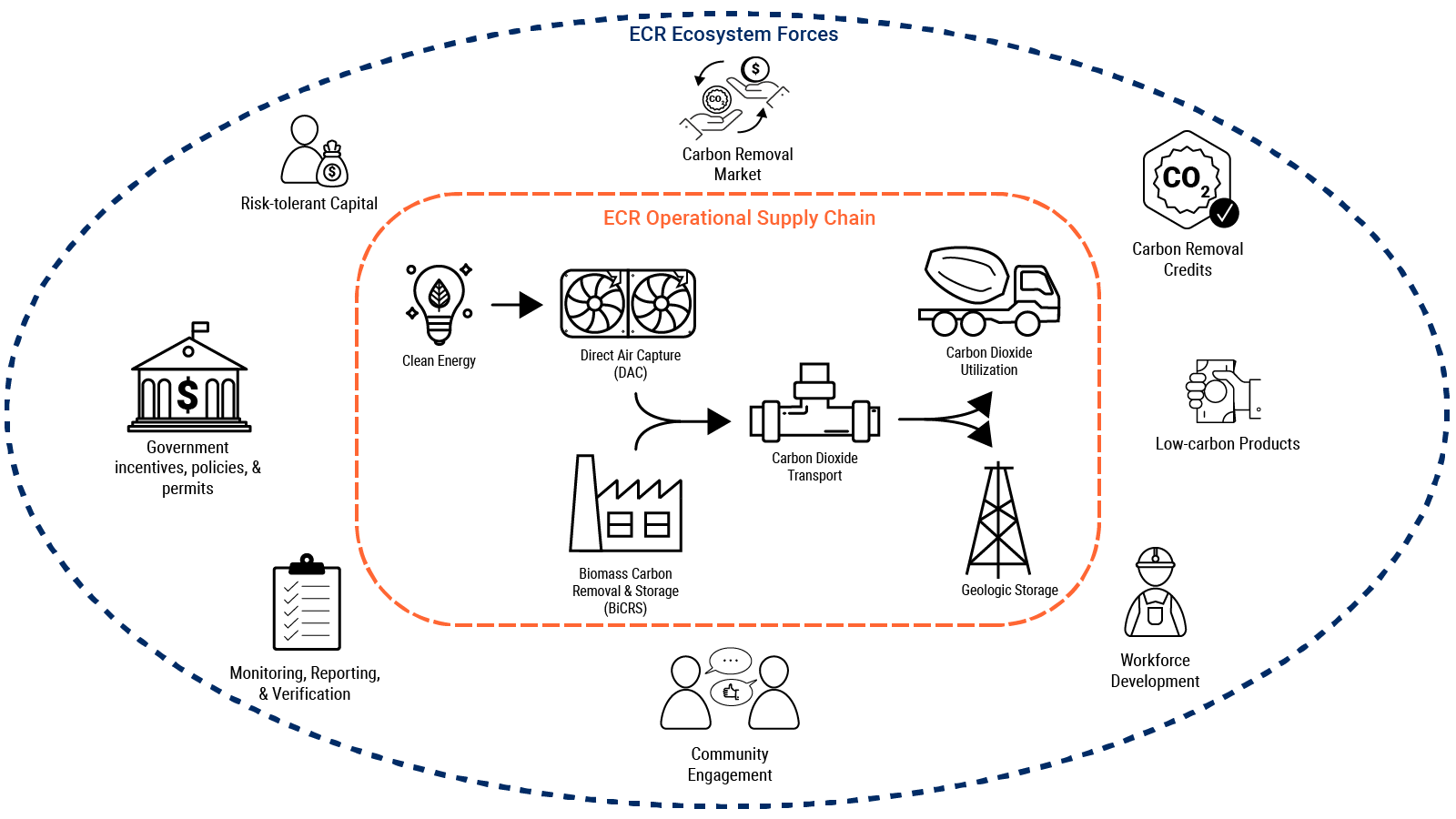

Engineered carbon removal is among a multitude of new, innovative technologies critical to meeting our long-term climate goals. Government and private businesses are developing groundbreaking policies and making record-breaking investments toward deploying them across the U.S. economy. As climate technologies move out of the lab and into the field, they’ll need demonstration projects to prove their full potential and limitations. Multiple U.S. projects are currently under construction.

The next decade should focus on the rapid dispersal of engineered carbon removal (ECR) and other critical-path climate technologies. Innovators will need to critically consider the technical, market, and policy actions needed to enable large-scale deployment and long-term commercialization. The C2ES Technology Working Groups support this challenge by providing a venue where the entire technology ecosystem can convene to address these topics.

The first of these working groups focuses on the deployment and commercialization of ECR, specifically, direct air capture and biomass carbon removal and storage (BiCRS).