Publication

Options and Considerations for a Federal Carbon Tax

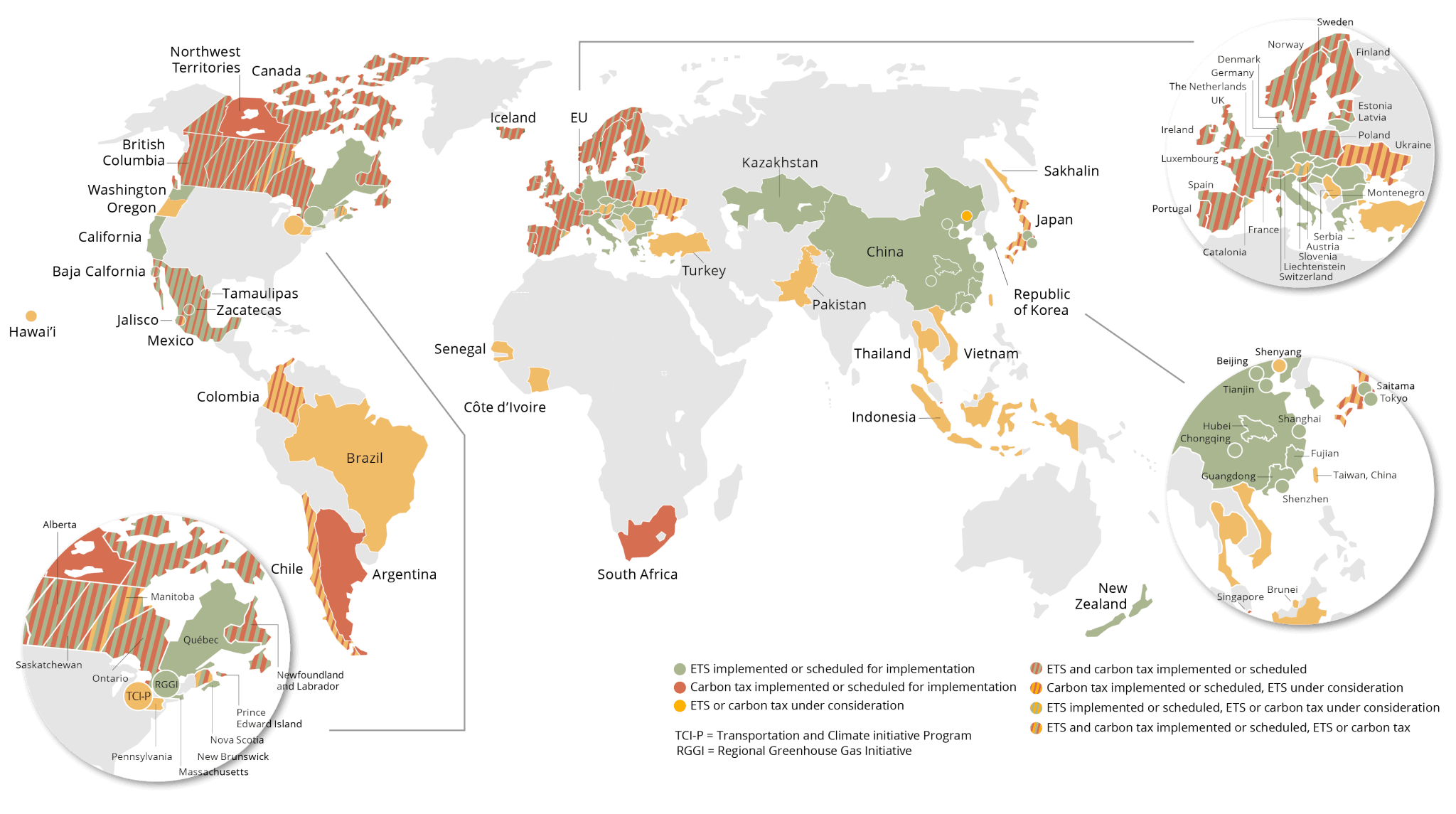

Greenhouse gas emissions can be reduced most cost-effectively through market-based […]

Under a carbon tax, the government sets a price that emitters must pay for each ton of greenhouse gas emissions they emit. Businesses and consumers will take steps, such as switching fuels or adopting new technologies, to reduce their emissions to avoid paying the tax.

A carbon tax differs from a cap-and-trade program in that it provides a higher level of certainty about cost, but not about the level of emission reduction to be achieved (cap and trade does the inverse).

Taxes on greenhouse gases come in two broad forms: an emissions tax, which is based on the quantity an entity produces; and a tax on goods or services that are generally greenhouse gas-intensive, such as a carbon tax on gasoline.

Several carbon tax proposals have been introduced in Congress in recent years. In the 118th Congress (2023–2024), two carbon pricing proposals have been introduced (as of January 2024), and several more are expected before the end of 2024.

Policymakers must consider a range of design choices, including:

Scope – The scope of the carbon tax depends on substances covered. For instance, a carbon tax could be levied on the carbon dioxide content of fossil fuels.

Point of Taxation – A carbon tax can be levied at any point in the energy supply chain. The simplest approach, administratively, is to levy the tax “upstream,” where the fewest entities would be subject to it (for instance, suppliers of coal, natural gas processing facilities, and oil refineries). Alternatively, the tax could be levied “midstream” (electric utilities) or downstream (energy-using industries, households, or vehicles).

Tax and Escalation Rates –Economic theory suggests a carbon tax should be set equal to the social cost of carbon, which is the present value of estimated environmental damages over time caused by an additional ton of carbon dioxide emitted today. The tax rate should also rise over time to reflect the growing damage expected from climate change. An increasing price over time also provides a signal to emitters that they will need to do more and that their investments in more aggressive technologies will be economically justified. One of the challenges of a carbon tax is forecasting the resulting level of emissions reduction from a specific tax rate. Building in review and opportunity for adjustment can help, but also reduces the one of the values of a carbon price—price certainty.

Distributional Impacts – Lower-income households spend a larger share of their income on energy than higher-income households. As a result, a price on carbon that increases energy costs can have a greater impact on lower-income individuals. Directing a certain percentage of revenue from a carbon tax toward low-income households to compensate for increased energy costs can help ensure that the tax does not disproportionately affect the poor.

Competitiveness – Without provisions protecting local production, a carbon price could put domestic energy-intensive, trade-exposed industries (EITEs), such as chemicals, cement/concrete, and steel, at a competitive disadvantage against international competitors that do not face an equivalent price. A shift in demand to those countries could result in “emissions leakage” from one country to another—reducing the climate benefit of a carbon price. All existing carbon pricing programs include mechanisms to address competitiveness concerns. These include allocations based on historical emissions, output-based allocations, exemptions for select sectors, and rebates. There is growing interest in a carbon border adjustment as a preferred approach to address emissions leakage and incentivize emission reductions.

Revenues – A carbon tax can raise significant revenue. How that revenue is used will ultimately be a political choice. Some or all of it could be returned to consumers in the form of a dividend. Alternatively, it could be reinvested in climate purposes, such as advancing low-carbon technologies or building resilience. Economic research suggests that using the revenues to reduce existing taxes on labor and capital—also known as a tax swap—can minimize the economic costs and may result in net economic benefits.

Last Updated May 2024