Carbon dioxide (CO2) is one of the building blocks of the Earth, but the rapidly growing concentration of it in the atmosphere threatens to alter the climate, bringing potentially devastating consequences. As we aim to limit the pace of climate change, we need to both emit less, and capture what we do emit. But if we capture it, then what do we do with all that CO2?

Geologic storage is a proven destination for excess CO2, but the notion of using carbon oxides (both CO2 and carbon monoxide, or CO) in commercial products and processes is an option that is gaining attention. Gaze around the room or out the window, and you’re looking at a lot of products containing carbon. Turning our waste carbon into more of those products could create a true “circular economy.” Problem solved, right?

Not quite yet, but the notion of carbon utilization (also known as carbontech or carbon recycling) is a step in the right direction. A new report from C2ES explores how utilization can put us on the path to more decarbonization options that also may offer substantial economic benefits. The C2ES report considers previous research conducted by the University of Michigan’s Global CO2 Initiative, the National Academies of Sciences, and others, and it lays out a policy roadmap for achieving the goals identified by those works. The conclusion: Adopting a suite of enabling policies now may encourage new markets to develop more quickly, and lead to greater positive climate impact later.

However, two challenges exist to ramping up markets for carbontech: The first is the “tech” part, where additional research and development (R&D) are needed to better develop these processes. The second is the market aspect: While using carbon to make products may be technically feasible, can it be done commercially? The challenges are closely related: In fact, the goal of R&D often may be simply reducing the cost of production.

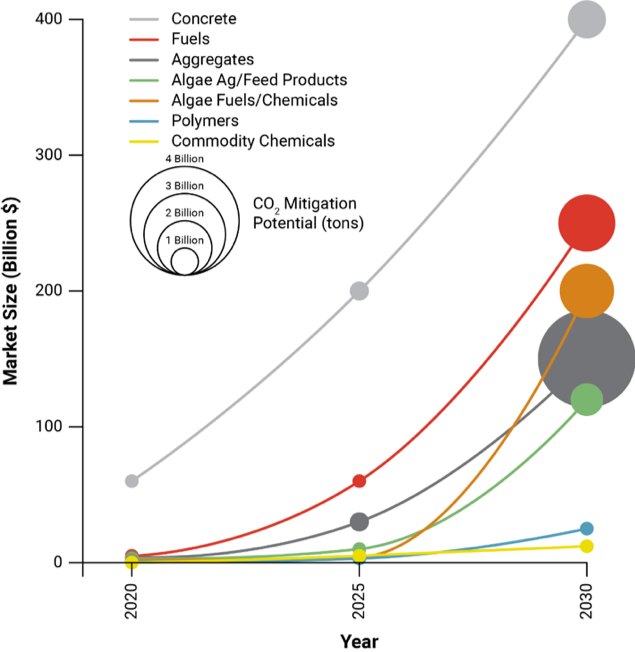

Carbontech products can be broadly grouped into these categories:

- Construction materials (e.g., cement and aggregate)

- Fuels/Chemicals/Polymers

- Algae-based products (e.g., feeds, fuels, fertilizers)

Each sector and sub-sector has its own distinct development pathway, including separate R&D challenges, market value, and potential to contribute to greenhouse gas reduction. Of these, creating carbon oxide-based construction materials face the fewest technical challenges. However, these new products face significant market resistance: Do they meet accepted building codes and performance standards? Other sectors, such as fuels, chemicals, and polymers face different R&D challenges, and also have relatively high potential climate benefits. Algae, which are known as “CO2 eating machines,” can produce the widest array of products.